Ohio businesses pay an average of $160 per month ($1,925 per year) for minimum coverage commercial auto insurance, based on MoneyGeek's analysis of eight vehicle types across 25 general industry categories. That puts Ohio just below the average commercial auto insurance cost national benchmark of $163 per month, making it one of the more moderately priced states in the country at rank 29 out of 51.

Among Ohio's neighboring states, Pennsylvania is the clear outlier at $79 per month, well below both Ohio and the national average. Indiana ($157), Kentucky ($155) and West Virginia ($152) all sit close to Ohio's figure, while Michigan ($312) runs nearly double the state's rate.

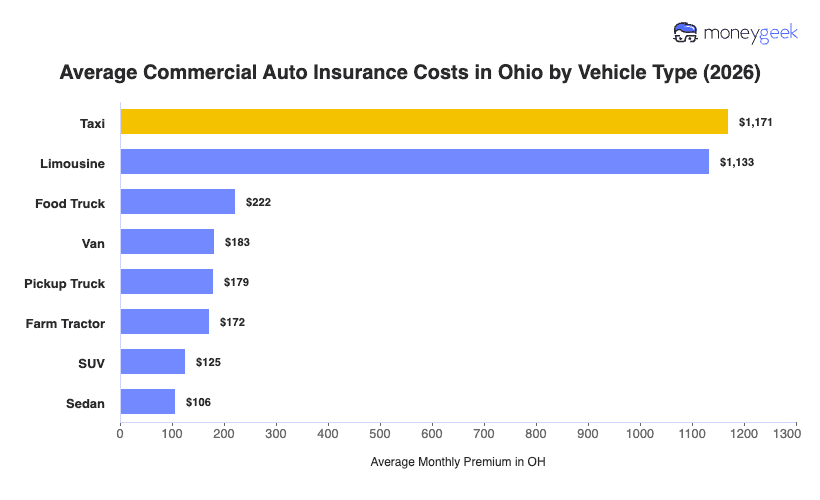

Ohio's commercial auto rates reflect a mix of urban density in markets like Columbus, Cleveland and Cincinnati, moderate litigation activity and claim costs that track close to national norms. Your commercial auto insurance rates will differ from that state benchmark depending on your vehicle, your drivers and what your business does.