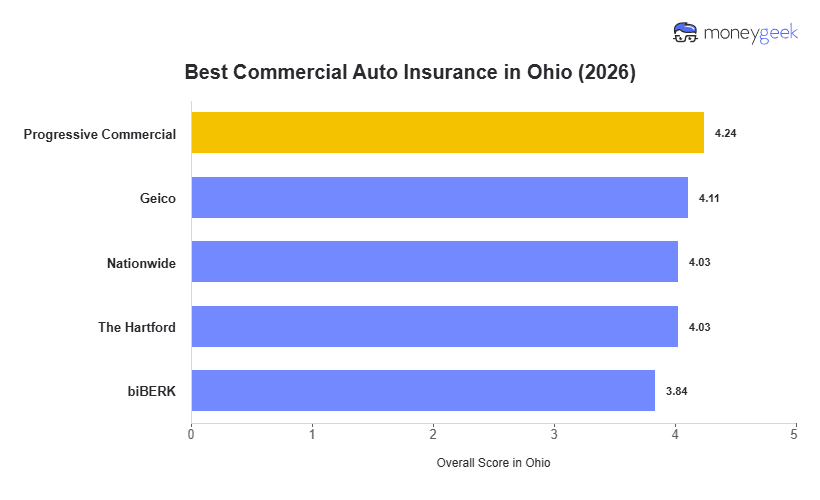

Commercial auto rates in Ohio vary more by vehicle type and industry than most business owners expect, which means the best commercial auto insurance decision comes down to three things specific to each operation: what vehicles it runs, what a serious claim would actually cost it and how much hands-on support it needs when something goes wrong. Progressive ranks first in Ohio overall, but a Cincinnati cleaning company running three sedans and a multi-truck construction fleet out of Akron are not shopping for the same policy.

Every provider on this list earned its spot for a reason that matters more than its rank when a business has a specific vehicle mix, industry risk profile or coverage priority:

- Progressive: Best Overall, Best for Fleet Operations

- GEICO: Best for Low-Risk Business Areas

- Nationwide: Best for Agricultural and Specialty Fleets

- The Hartford: Best for Coverage Depth

- biBerk: Best for Simple Coverage Needs

The table below puts all five providers side by side for a direct comparison.