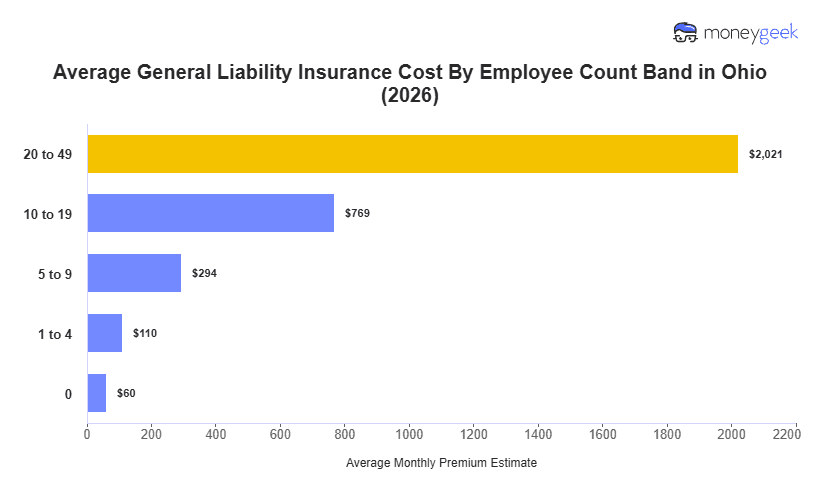

The average cost of general liability insurance in Ohio is $110 per month, or $1,322 annually, for businesses with one to four employees. This sits 10% below the national average, ranking Ohio 22nd nationally for affordability.

Ohio's pricing aligns more closely with lower-cost neighbors than regional outliers. Kentucky and Indiana both run cheaper at $102 and $106 monthly, while Pennsylvania tracks higher at $129. Within the Midwest, Ohio sits nearer the median alongside Wisconsin ($108) and Michigan ($115), but well below Illinois ($141), the region's cost outlier. The state's below-average pricing reflects competitive market conditions and a moderate risk environment relative to the national baseline.

Treat Ohio's monthly average as a starting reference, as your actual premium will shift based on your industry's risk profile, payroll size, and claims history. Use this figure to assess whether quotes you receive cluster near the typical range or land meaningfully higher.