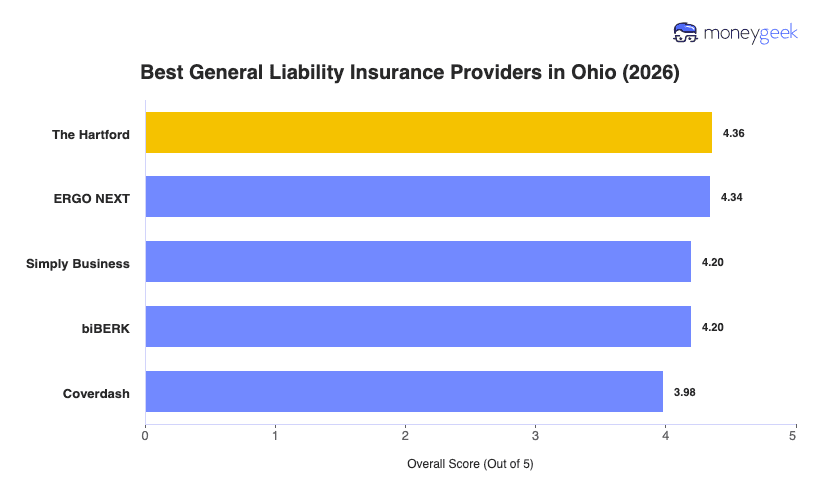

The best general liability insurance companies for Ohio small businesses balance competitive rates with dependable claims handling and flexible coverage options. These five ranked highest in MoneyGeek's analysis of 10 major insurers across 25 industries, evaluated at $1 million per occurrence/$2 million aggregate limits:

- The Hartford: Best Overall, Best for Service and Care Industries

- ERGO NEXT: Best for Customer Experience

- Simply Business: Best for Multiple Carriers Comparisons

- biBERK: Best for Service Businesses

- Thimble: Best for Seasonal Businesses

These insurers are well-matched to Ohio's small business market, covering seasonal operations with winter weather exposure and year-round service businesses. Each is detailed below, including where the fit is strongest.