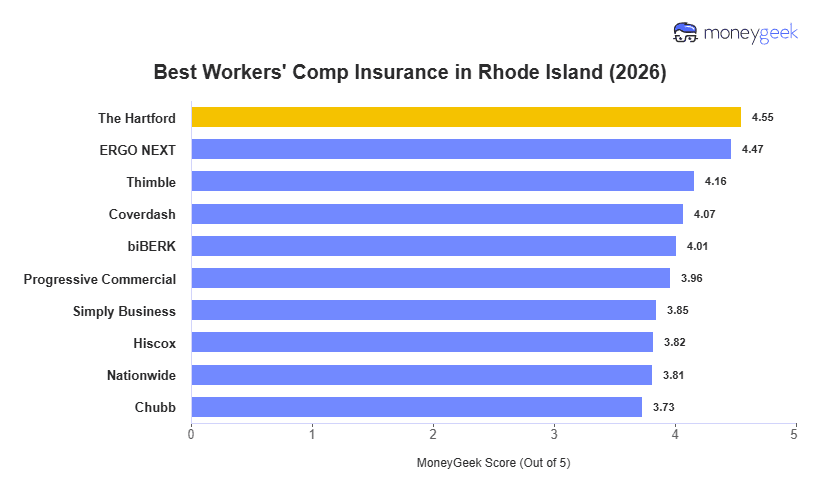

The Hartford ranks first among workers' comp insurance providers in Rhode Island at $94 per month, with strong customer experience and coverage scores. ERGO NEXT matches that rate at $94 per month and leads all Rhode Island providers on customer experience with a fully digital buying process.

Thimble ranks third at $104 per month, a strong fit for small businesses that need flexibility and fast coverage management. Thimble's platform lets businesses adjust coverage, generate certificates and manage policies online without agent involvement, making it a practical choice for contractors, freelancers and seasonal businesses.