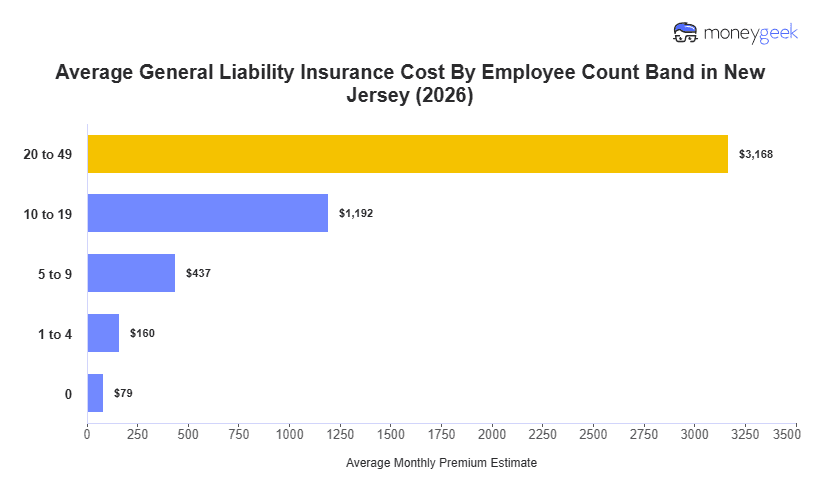

New Jersey ranks as the fourth most expensive state for general liability insurance, with businesses employing one to four people paying an average of $160 monthly ($1,916 annually).

General liability costs in New Jersey are $37 above the national average and in the upper tier of a regional cluster: Pennsylvania sits at $129, while New York is at $180. The $51 spread across these three neighboring states reflects differences in litigation costs and claims density rather than sharp state-by-state breaks.

Delaware averages $131 a month, clustering with Pennsylvania at the low end of the neighboring-state range. New Jersey sits well above both.

Commercial density and legal environment drive New Jersey's costs higher than most neighbors, short of New York.

New Jersey’s average captures premium estimates across over 400 business types in MoneyGeek's statewide analysis. Individual quotes vary depending on your industry's exposure profile, annual revenue, claims record and coverage structure.

Use the state average to gauge whether your pricing aligns with typical New Jersey costs, then identify which business-specific factors explain any gap.