MoneyGeek analyzed quotes from over 400 business types in New Jersey and found five of the best general liability insurance companies, balancing affordability, customer service and coverage options:

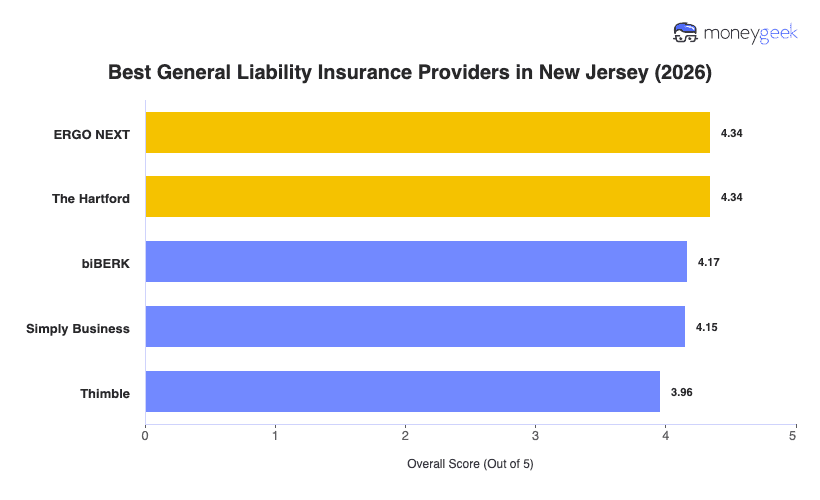

Both ERGO NEXT and The Hartford share the score for best overall.

- ERGO NEXT: Best for Hands-On Industries

- The Hartford: Top for Professional Services

- biBerk: First for Service-Based Businesses

- Simply Business: Best for Comparing Multiple Carriers

- Thimble: Ranks first for On-Demand and Project-Based Coverage

Each of these insurers offers New Jersey businesses competitive pricing, responsive service and flexible coverage structures. The table shows how they stack up against each other and which one might work best for your specific operation and risk profile.