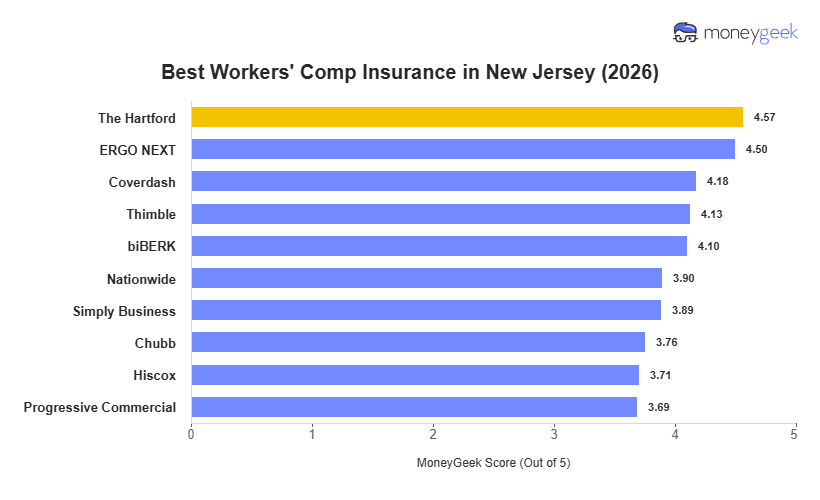

New Jersey is one of the highest-cost workers' comp markets in the country, with an average rate of $186/month per employee. The Hartford has the best workers' comp insurance in the state and the lowest price at $137/month. ERGO NEXT trails by $1/month and has the best customer experience in New Jersey.

The $104/month spread between the cheapest and most expensive providers in our analysis adds up quickly. For New Jersey employers with four employees, this difference reaches $4,992 annually.