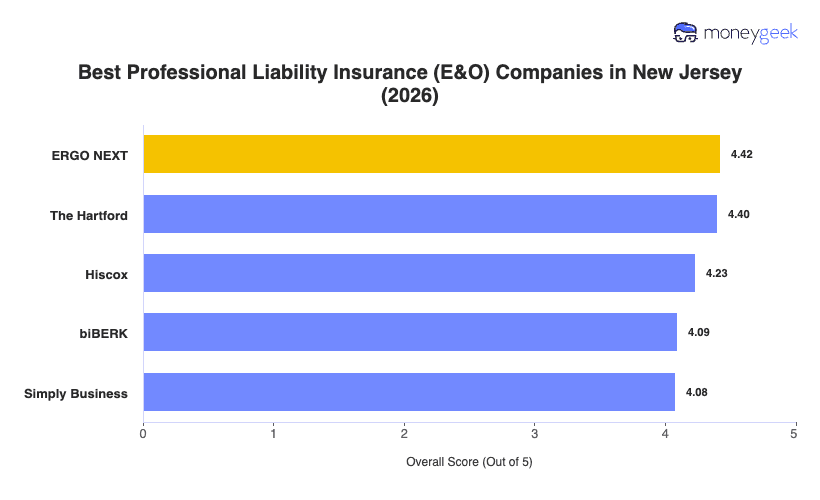

Our analysis of New Jersey professional liability insurers identified three providers that consistently outperformed the field on coverage quality, customer experience and overall fit for the state's service economy.

- ERGO NEXT: A fully digital buying experience and coverage spanning the widest range of New Jersey industries earned ERGO NEXT the top position. The insurer ranks first in the state across arts and media, childcare, construction and contracting, fitness, health care, other professional services, pet care, recreation and tech, making it a strong fit for small businesses across most of New Jersey's service economy.

- The Hartford: For New Jersey businesses in consulting, financial services, real estate and marketing, The Hartford ranks first in the state on overall score. Its professional liability policies can be bundled with a business owner's policy, and coverage extends across both the US and Canada, which suits the many New Jersey businesses with clients on both sides of the border. Healthcare and medical professionals should compare other options, as The Hartford ranks ninth in New Jersey for that industry, and the same applies to other professional services.

- Hiscox: Founded in 1901, Hiscox brings more than 120 years of specialty insurance experience to New Jersey businesses that need precise, industry-tailored coverage. The insurer covers more than 180 professions and ranks first in the state for nonprofits and associations, with strong performance in consulting, financial services and beauty and wellness.

Ranked providers represent the best fit for most New Jersey businesses, but no single list accounts for every profession, client type or coverage need. Comparing business insurance options side by side and getting quotes directly from carriers gives you the most complete picture before making a final decision.