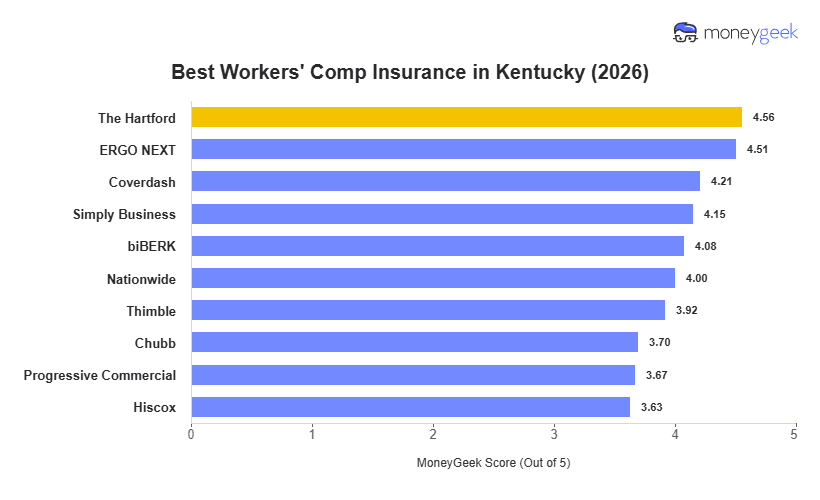

The Hartford leads Kentucky workers' comp insurance with the top MoneyGeek score, combining strong claims performance with the second-lowest rate in the state. ERGO NEXT ranks second at $56/month, $3 below The Hartford, and holds the highest customer experience score in the state.

The $50 spread from ERGO NEXT to Chubb gives Kentucky employers a meaningful rate range to shop against, but the gap between provider rates narrows in construction, agriculture, and transportation class codes.