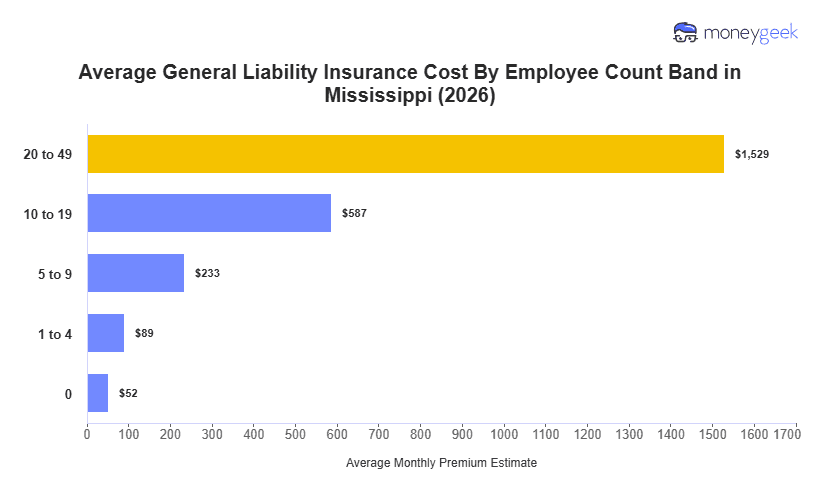

General liability insurance in Mississippi averages $89 per month, or $1,074 annually, for small businesses with one to four employees. For that profile, Mississippi falls 27% below the national average of $123 monthly and ranks as the second most affordable state for general liability insurance costs. Treat this as a benchmark as actual pricing shifts with industry, coverage limits and claims history.

Compared to adjacent states, Mississippi runs $11 to $23 cheaper per month than Alabama ($100), Louisiana ($106), and Tennessee ($112). The entire Southeast trends below the national average, likely due to lower claim costs, reduced litigation exposure and a higher share of lower-risk small businesses. Mississippi anchors the low end of an already-affordable regional cluster.

A quote near the state benchmark suggests typical positioning for a Mississippi small business. Quotes landing above that range raise a diagnostic question: which factor is driving the gap? A Mississippi general liability insurance cost calculator is available below for a more personalized estimate.