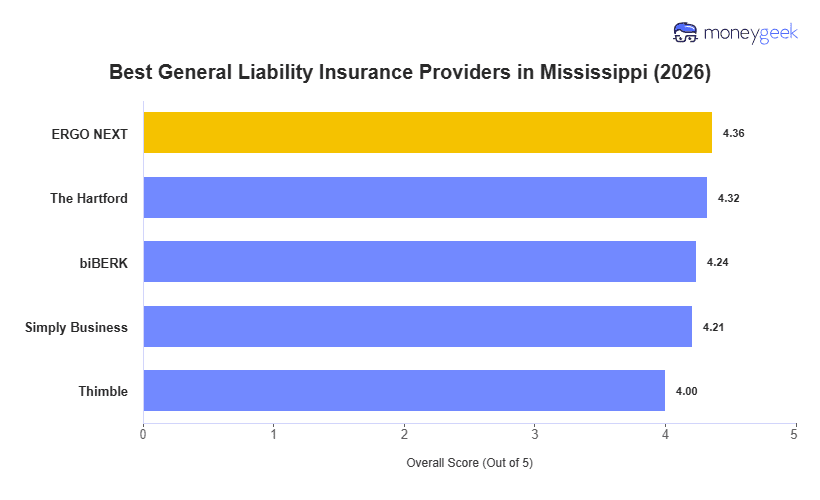

Not every insurer fits every Mississippi business, and low rates alone don't guarantee the right coverage. We analyzed policies with $1 million/$2 million limits across 408 business types and identified five insurers that consistently provide value across industries. These are the best and cheapest options for small businesses in the state:

- ERGO NEXT: Best Overall, Best for Hands-On and Service Industries

- The Hartford: Best Cheap General Liability Insurance

- biBerk: Best for Service and Recreation Businesses

- Simply Business: Best for Comparing Multiple Carriers

- Thimble: Best for Short-Term and Project-Based Coverage

Mississippi's mix of agriculture, manufacturing, and tourism means risk profiles vary widely across the state. The table breaks down each provider's rankings and estimated rates, so a shrimp boat operation in Biloxi and a machine shop in Tupelo can compare options that fit their exposure and budget.