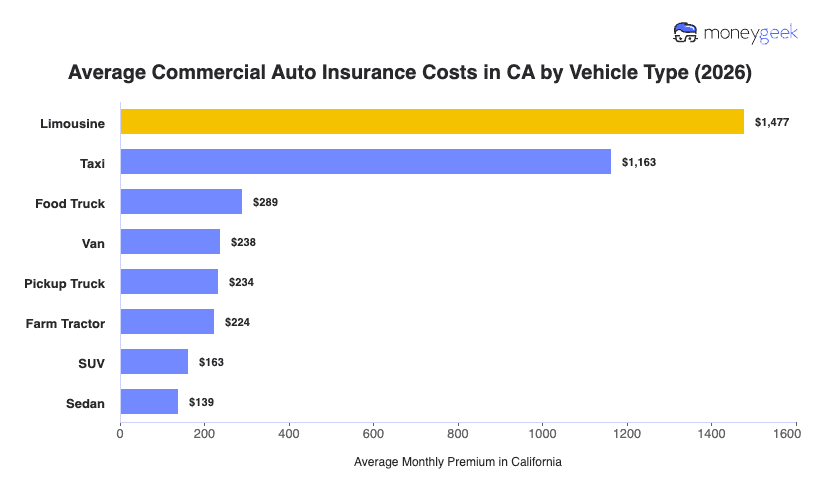

The average commercial auto insurance cost for California businesses is $209 per month ($2,503 per year) for minimum coverage, based on MoneyGeek's analysis of eight vehicle types across 25 general industry categories. That puts California 28% above the average commercial auto insurance cost of $163 per month nationally, ranking 44th out of 51 states for affordability.

California's rates run higher than every neighboring state. Oregon comes closest at $158 per month, followed by Washington at $157, Nevada at $167 and Arizona at $149. None of the states bordering California come close to its $209 monthly average.

Three factors push California above the national benchmark: an active litigation climate with higher attorney involvement and larger jury awards than most markets, dense urban centers like Los Angeles and San Francisco with higher claim frequency and repair costs, and the January 2025 minimum liability increase to 30/60/15. Your rate will differ from that benchmark depending on your vehicle, your drivers and what your business does.