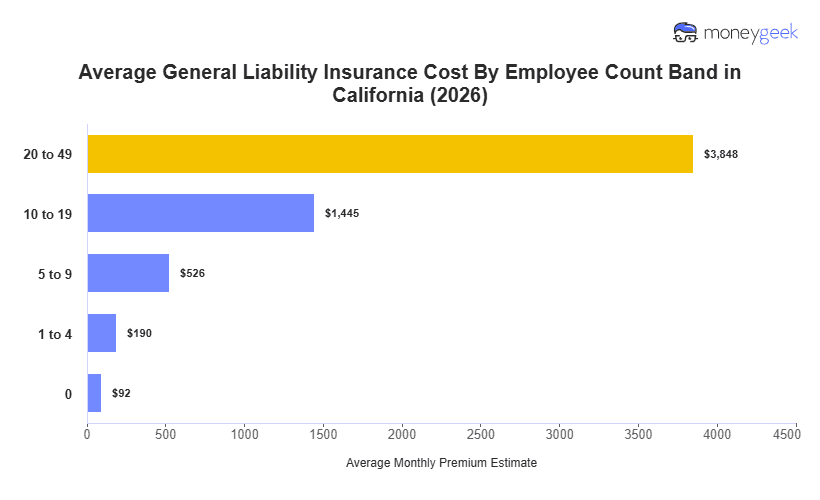

For most California small businesses, their general liability insurance rates will be the most expensive in the United States at an average of $190 monthly ($2,285 annually) sitting at 54% higher than national benchmarks. This represents small companies with 1 to 4 employees and limits of $1 million per occurrence/$2 million aggregate.

Even neighboring states and others in the same region don't come close to California's average. Washington is the nearest at $152 a month. California's closest pricing comparisons are actually with states on the opposite coast: Washington D.C., New York, Massachusetts and New Jersey.

Keep in mind that our pricing is only a state benchmark and should not be treated as a quote you'll receive. Your actual pricing will mostly depend on your industry area and your business size, among other factors within your operating location to consider.

The California general liability insurance cost calculator below can help you get a more personalized estimate.