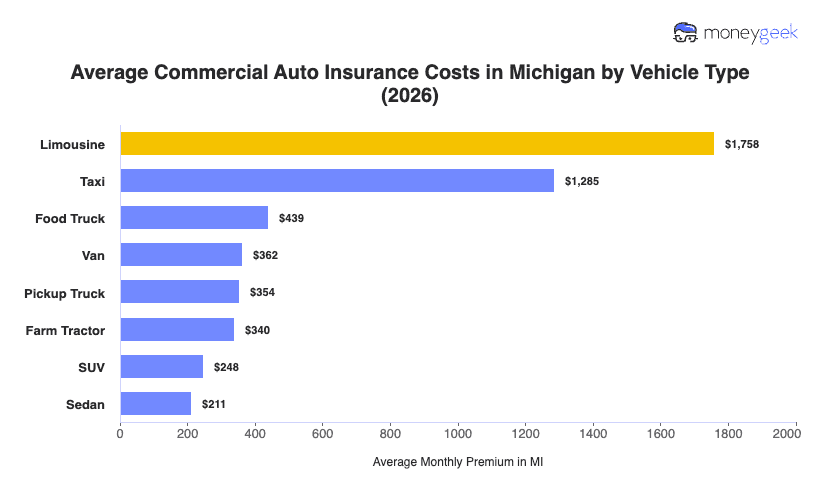

Michigan's average commercial auto insurance cost for minimum coverage is $312 per month ($3,746 per year), based on MoneyGeek's analysis of eight vehicle types across 25 general industry categories. Michigan ranks 51st nationally, putting it $149 above the national benchmark of $163 per month and well above every neighboring state in the region.

Among nearby states, Illinois comes closest to the national average at $179 per month, while Ohio ($160) and Indiana ($157) run closer to the benchmark. Wisconsin, at $119 per month, is the most affordable of Michigan's neighbors and costs $193 less per month than Michigan.

Michigan's commercial auto rates are driven by the state's unique no-fault insurance law, high litigation rates and above-average claim costs in dense urban markets like Detroit and Grand Rapids. Your commercial auto insurance rates will differ from that state benchmark depending on your vehicle, your drivers and what your business does.