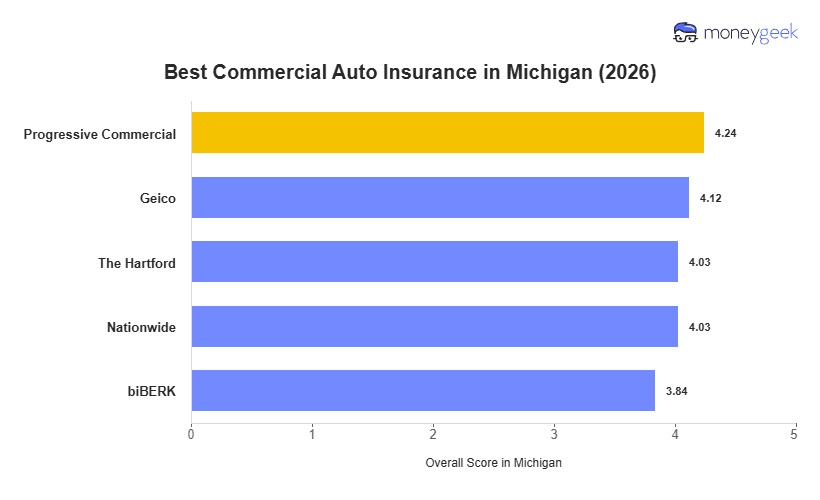

No single insurer is the right best commercial auto insurance option for every Michigan business. Progressive Commercial leads overall, but the right carrier depends on three things specific to the operation: what vehicles the business operates, what a serious claim would cost the business and how much support it needs when something goes wrong. A concrete hauler running a fleet of dump trucks through Wayne County will reach a very different conclusion than a solo consultant driving a leased sedan between Ann Arbor and Detroit.

Each provider below earned its place for a distinct reason, and that reason matters more than its position on the list when a business has a specific vehicle profile, risk level or set of priorities:

- Progressive Commercial: Best Overall, Best for Fleet Operations

- GEICO: Best for Low-Risk Business Areas

- The Hartford: Best for Coverage Depth

- Nationwide: Best for Agricultural and Specialty Fleets

- biBERK: Best for Simple Coverage Needs

The table below shows how all five ranked across Michigan for a side-by-side view to ground the comparison.