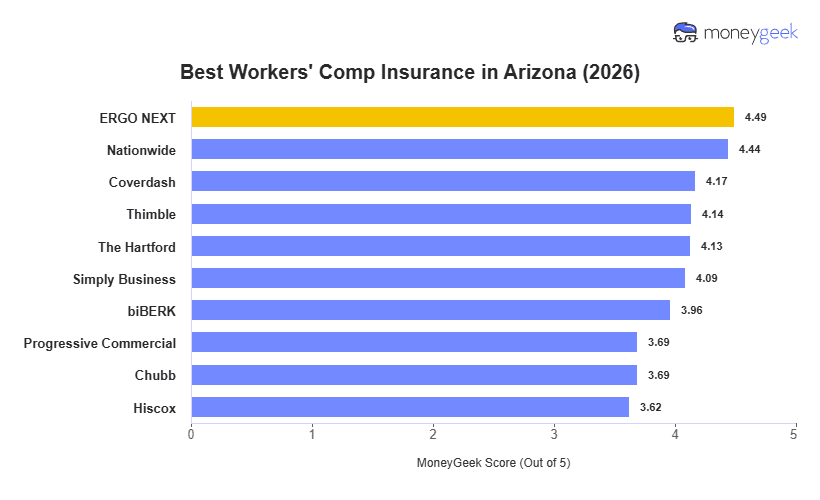

ERGO NEXT is the best workers' compensation insurance provider in Arizona. ERGO NEXT and Nationwide both come in at $65 per month, the lowest rate in our analysis, yet land on opposite ends of the customer service rankings. If rate is your only priority, either works. But if a claim ever arises, that service gap matters.

The rate difference between the cheapest and most expensive provider is $57 per month, from $65 with ERGO NEXT and Nationwide to $122 at Chubb. For a small Arizona employer, that's $684 per year for base coverage. Whether that premium difference buys better coverage depends on the provider's available endorsements.