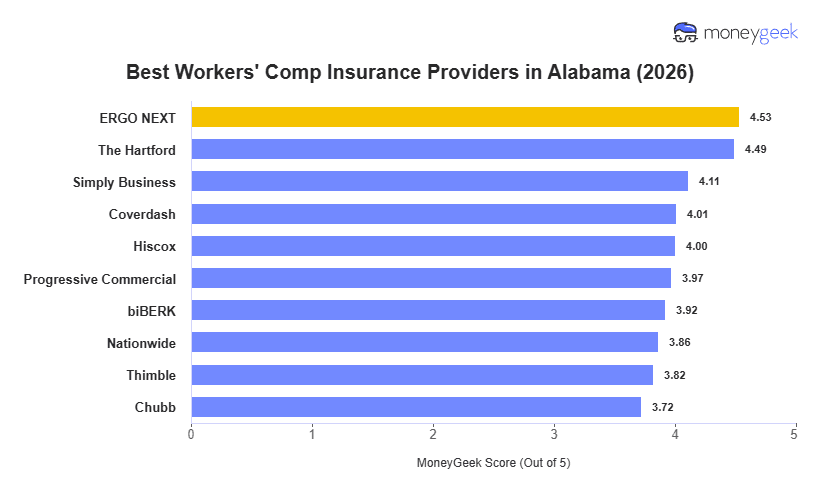

ERGO NEXT has the best worker's comp insurance in Alabama, with top rankings for affordability and customer experience. The Hartford follows as a close runner-up with competitive rates and above-average claims performance. Both are worth evaluating for workers' comp insurance depending on your industry and risk profile.

One interesting fact we found in our data is that the monthly rate spread between ERGO NEXT at $54 and Chubb at $96 is $42 per employee. That gap is most meaningful for small businesses with lean payroll budgets in low-hazard industries. Employers where claims handling in complex industries is the priority may find a higher-cost provider the stronger fit.