ERGO NEXT leads our research for the best workers' comp insurance in Utah with strong customer support, competitive rates and broad coverage options. For employers weighing alternatives, Coverdash and The Hartford are strong runner-up options with competitive rates and reliable coverage.

Best Workers' Comp Insurance in Utah (2026)

With rates starting at $9 monthly, ERGO NEXT, Coverdash and The Hartford offer the cheapest and best workers' comp insurance in Utah.

Get matched to top Utah workers' comp insurance providers and find your ideal coverage.

Select state

Updated: June 30, 2026

Advertising & Editorial Disclosure

ERGO NEXT is Utah's cheapest workers' comp provider at $54 a month and is also our top pick for the best workers' comp insurance in the state. The five most affordable providers are:

- ERGO NEXT: $54 a month

- Thimble: $61 a month

- Coverdash: $66 a month

- Nationwide: $68 a month

- The Hartford: $72 a month

Utah mandates workers' comp insurance for most employers with one or more employees, including part-time workers. Exemptions include sole proprietors without employees, partners and corporate officers owning 10% or more of company stock. Noncompliance results in fines up to $1,000 per employee plus daily penalties until coverage begins.

Utah's average workers' comp insurance cost is $73 a month per employee. The cheapest industry is Beauty, Body and Wellness Services at $13 a month, while the most expensive is Transportation and Logistics at $219 a month.

You can get workers' comp coverage in Utah by:

- Purchasing from private insurance companies licensed to sell workers' comp in Utah

- Buying through the Workers' Compensation Fund of Utah, the state-operated insurer

- Self-insuring if your business meets Utah's strict financial requirements and approval process

Many business owners compare quotes online or through brokers to get the best rate and compliance support.

Workers’ compensation in Utah covers:

- Medical expenses for work-related injuries, from minor cuts at Salt Lake City construction sites to serious machinery accidents in Provo factories

- Wage replacement benefits providing partial income during recovery periods

- Permanent disability compensation for lasting impairments that affect earning capacity

- Survivor benefits for families when workplace fatalities occur, including funeral costs and ongoing financial support

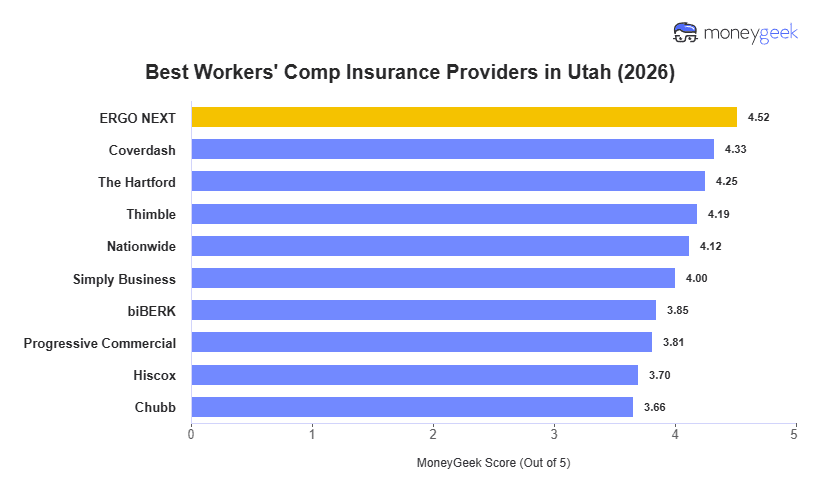

Best Workers' Comp Insurance Companies in Utah

| ERGO NEXT | 4.52 | $54 | 1 | 6 |

| Coverdash | 4.33 | $66 | 5 | 1 |

| The Hartford | 4.25 | $72 | 3 | 3 |

| Thimble | 4.19 | $61 | 8 | 9 |

| Nationwide | 4.12 | $68 | 6 | 5 |

| Simply Business | 4.00 | $77 | 2 | 2 |

| biBERK | 3.85 | $75 | 8 | 8 |

| Progressive Commercial | 3.81 | $76 | 8 | 7 |

| Hiscox | 3.70 | $80 | 6 | 10 |

| Chubb | 3.66 | $99 | 3 | 4 |

How Did We Determine These Rates and Rankings?

These rates are estimates based on MoneyGeek's analysis of small businesses with 1 to 4 employees across 408 major industries. Actual rates vary based on your business location, industry risk factors, claims history, coverage limits and individual insurer underwriting criteria. Contact insurers directly for personalized quotes.

ERGO NEXT

Best Workers' Comp Insurance in Utah

MoneyGeek Rating

4.5/ 5

5/5Affordability Score

4.3/5Customer Experience Score

3.5/5Coverage Score

Average Monthly Cost

$54Claims Processing Score

4/5Policy Management Score

4.1/5Buying Process Score

4.4/5

Coverdash

Best Utah Workers' Comp Insurance: Runner-Up

MoneyGeek Rating

4.3/ 5

4.5/5Affordability Score

4/5Customer Experience Score

5/5Coverage Score

Average Monthly Cost

$66Claims Processing Score

4/5Policy Management Score

4/5Buying Process Score

4/5

LEARN MORE ABOUT UTAH BUSINESS INSURANCE

Cheapest Workers' Comp Insurance Companies in Utah

ERGO NEXT has the cheapest workers’ compensation insurance in Utah at $54 monthly per employee ($648 annually). Thimble is the next cheapest option at $61 monthly, followed by Coverdash at $66.

The pricing gap between providers can meaningfully affect small business costs. The difference between ERGO NEXT ($54) and The Hartford ($72) amounts to roughly $216 more annually per employee, while the gap between ERGO NEXT and Chubb ($99), Utah’s most expensive provider in our analysis, grows to about $540 annually per employee.

| ERGO NEXT | $54 | $648 |

| Thimble | $61 | $732 |

| Coverdash | $66 | $792 |

| Nationwide | $68 | $816 |

| The Hartford | $72 | $864 |

| biBERK | $75 | $900 |

| Progressive Commercial | $76 | $912 |

| Simply Business | $77 | $924 |

| Hiscox | $80 | $960 |

| Chubb | $99 | $1,188 |

Cheapest Workers' Comp Insurance in Utah by Industry

ERGO NEXT offers the lowest workers’ compensation rates in 18 of the 25 Utah industries analyzed, with its biggest pricing advantages appearing in higher-risk industries. The Hartford provides the cheapest rates in six lower-risk, office-focused industries.

ERGO NEXT's rates range from $10 per month for marketing firms to $126 for construction contractors. Thimble offers the lowest rate for other professional services at $15 per month. Businesses with less traditional classifications should compare quotes across multiple providers before choosing coverage.

| Financial Services | The Hartford | $9 | $108 |

| Beauty, Body & Wellness Services | ERGO NEXT | $10 | $120 |

| Marketing & Communications | ERGO NEXT | $10 | $120 |

| Consulting Services | The Hartford | $11 | $132 |

| Real Estate & Property Services | The Hartford | $12 | $144 |

| Other Professional Services | Thimble | $15 | $180 |

| Childcare Services | ERGO NEXT | $22 | $264 |

| Food & Beverage | ERGO NEXT | $23 | $276 |

| Tech/IT | The Hartford | $23 | $276 |

| Hospitality, Travel & Tourism | The Hartford | $25 | $300 |

| Healthcare & Medical | The Hartford | $27 | $324 |

| Retail & Product Rental | ERGO NEXT | $30 | $360 |

| Nonprofit & Associations | ERGO NEXT | $34 | $408 |

| Pet Care Services | ERGO NEXT | $34 | $408 |

| Education | ERGO NEXT | $38 | $456 |

| Fitness Services | ERGO NEXT | $38 | $456 |

| Repair & Maintenance | ERGO NEXT | $40 | $480 |

| Arts, Media & Entertainment | ERGO NEXT | $53 | $636 |

| Recreation & Sports | ERGO NEXT | $60 | $720 |

| Cleaning Services | ERGO NEXT | $62 | $744 |

| Manufacturing | ERGO NEXT | $81 | $972 |

| Agriculture & Natural Resources | ERGO NEXT | $88 | $1,056 |

| Wholesale & Distribution | ERGO NEXT | $102 | $1,224 |

| Construction & Contracting | ERGO NEXT | $126 | $1,512 |

| Transportation & Logistics | ERGO NEXT | $161 | $1,932 |

How Much Is Workers' Comp Insurance in Utah?

Utah’s workers’ compensation rates average about $73 monthly per employee, close to the national average. But costs vary dramatically by industry, ranging from roughly $13 to $219 depending on the type of work employees perform.

Our analysis found that pricing increases quickly as workplace injury risk rises. Even industries many employers consider relatively low risk, such as pet care services ($46 a month) and fitness services ($49 a month), still fall well above industries like marketing ($13) and financial services ($14).

Utah’s competitive insurance market helps keep rates lower for office-based businesses, but costs rise sharply in physically demanding industries. Construction and transportation businesses average about $210 monthly per employee, nearly three times the statewide average.

| Beauty, Body & Wellness Services | $13 | $156 |

| Marketing & Communications | $13 | $156 |

| Financial Services | $14 | $168 |

| Consulting Services | $16 | $192 |

| Real Estate & Property Services | $18 | $216 |

| Other Professional Services | $20 | $240 |

| Childcare Services | $27 | $324 |

| Food & Beverage | $29 | $348 |

| Hospitality, Travel & Tourism | $31 | $372 |

| Tech/IT | $33 | $396 |

| Healthcare & Medical | $37 | $444 |

| Retail & Product Rental | $39 | $468 |

| Nonprofit & Associations | $42 | $504 |

| Pet Care Services | $46 | $552 |

| Fitness Services | $49 | $588 |

| Education | $50 | $600 |

| Repair & Maintenance | $53 | $636 |

| Arts, Media & Entertainment | $68 | $816 |

| Recreation & Sports | $83 | $996 |

| Cleaning Services | $86 | $1,032 |

| Manufacturing | $102 | $1,224 |

| Agriculture & Natural Resources | $119 | $1,428 |

| Wholesale & Distribution | $130 | $1,560 |

| Construction & Contracting | $201 | $2,412 |

| Transportation & Logistics | $219 | $2,628 |

Utah Workers' Comp Insurance Cost Factors

Utah workers' comp rates are set in a private competitive market regulated by the Utah Insurance Department and classified using NCCI class codes. One distinguishing cost driver in Utah is the absence of a state fund, which means all pricing competition occurs among private carriers.

How Much Workers' Comp Insurance Do I Need in Utah?

Utah law requires workers' compensation coverage for all employers with employees, with few exceptions. Your policy must provide medical benefits for life, temporary total disability benefits at 66-2/3% of average weekly wages, and death benefits for dependents.

Failing to maintain required workers' comp coverage results in penalties of $1,000 or three times the premium you would have paid, whichever is greater. Each day without coverage constitutes a separate criminal offense.

Utah Workers' Comp Insurance Exemptions

Utah requires most businesses to have workers' comp coverage. These business categories are exempt:

- Domestic Workers: You're exempt if you employ domestic workers for fewer than 40 hours per week. This applies whether you hire one household employee or several workers who don't reach 40 hours combined each week.

- Agricultural Employers: Utah exempts farm operations that employ five or fewer non-family workers for at least 40 hours per week during any 13-week period in the past year. You're also exempt if only immediate family members who own part of the farm work there.

- Corporate Directors and Officers: Your Utah corporation can exclude up to five directors or officers from coverage if they're your only workers. Construction contractors and businesses that subcontract work don't qualify.

- Owner-Operator Truck Drivers: If you own or lease your vehicle and drive under an independent contractor agreement, Utah requires proof of occupational accident insurance instead of workers' comp coverage.

- Business Owners Without Employees: Sole proprietors with no employees can skip workers' comp by filing an annual Workers' Compensation Coverage Waiver with the Utah Labor Commission. Partners in a partnership with no employees outside the partnership can also waive coverage this way.

- LLC Members: Your LLC can waive coverage if members are your only workers. Utah has one exception: construction trade LLCs must carry coverage for all members regardless of employee count.

- Independent Contractors: Independent contractors can get a coverage waiver in Utah by proving they control how work gets done, aren't supervised daily and work on specific projects rather than ongoing employment.

- Volunteers: Nonprofits don't need coverage for volunteers unless they choose to provide it. Government entities may need to provide medical benefits to volunteers in some situations.

- Real Estate Professionals: Self-employed real estate agents don't usually need coverage, though requirements vary based on your work arrangement and whether you employ other agents.

FEDERAL WORKERS' COMP PROGRAMS OVERRIDE STATE REQUIREMENTS

Federal workers' comp programs apply to specific employee categories regardless of Utah state law. The Federal Employees' Compensation Act (FECA) covers federal civilian employees. The Federal Employers' Liability Act (FELA) covers railroad workers. The Longshore and Harbor Workers' Compensation Act covers maritime workers. Utah employers with employees in these categories must comply with the applicable federal program.

How to Get the Best Workers' Comp Insurance in Utah

Follow these steps to obtain the best workers' comp insurance for your Utah business. For a full walkthrough, see our guide on how to get workers' compensation insurance.

- 1

Confirm Utah Coverage Requirements

Verify your coverage obligations with the Utah Labor Commission and Utah Insurance Department before buying a policy. Most Utah employers with one or more employees must carry workers' comp. Confirm whether any exemptions apply to your business.

- 2

Identify Your NCCI Class Codes Accurately

Utah uses NCCI class codes to classify employees by job duty. Accurate classification is determines your base rate. Review your business operations and assign the correct codes for each employee category. Misclassification can trigger audit adjustments and changes to your premium.

- 3

Document Payroll, Employee Count and Claims History

Collect current payroll figures, total employee count and a five-year claims history before requesting quotes. Carriers use this data to calculate your premium and assess risk. Clean claims history and accurate payroll documentation can improve your pricing.

- 4

Request Quotes From Multiple Licensed Utah Carriers

Pull quotes from at least three licensed private carriers operating in Utah's competitive market. ERGO NEXT, Coverdash, The Hartford and other top-ranked providers all offer direct or online quoting. The Utah Insurance Department maintains a list of licensed carriers to confirm a provider's authorization.

- 5

Compare Total Value, Not Just Monthly Rate

Evaluate each quote on coverage completeness, claims support quality, policy flexibility and financial strength in addition to monthly rate. The $18 per month spread between Utah's cheapest provider, ERGO NEXT at $54 per month, and The Hartford at $72 per month, can be offset by differences in claims handling speed and loss-control resources.

- 6

Complete Purchase and Establish Payroll and Audit Reporting

After selecting a carrier, complete the application and bind coverage before your required effective date. Set up payroll reporting right away. Most Utah workers' comp policies are audited annually, and accurate payroll reporting throughout the policy year prevents large audit adjustments at renewal.

- 7

Review at Annual Renewal

Before each annual renewal, audit class codes, payroll figures and coverage limits for accuracy. Changes in employee count, job duties or claims history can affect the renewal rate. Pull competing quotes from multiple Utah carriers at renewal to confirm you still have the best available rate.

Bottom Line

ERGO NEXT is the best workers' comp provider for most Utah employers, combining the state's lowest rate with the top overall MoneyGeek score. Coverdash is a reliable alternative for small businesses that prioritize a fast digital buying experience, while The Hartford suits employers who need deeper claims support and loss-control resources. The right choice for your business depends on your industry, claims history and how much weight you place on price versus service depth.

Next Steps

Utah workers' comp rates vary by NCCI class code, so your actual premium may differ from the state average. Use these resources to move forward with confidence.

Utah Workers' Compensation Insurance FAQs

Utah employers who fail to carry required coverage face fines and potential stop-work orders issued by the Utah Labor Commission.

Utah workers' comp covers employees whose work is principally located in Utah. Remote employees who work primarily in another state may require coverage under that state's workers' comp laws. Employers with workers in multiple states should notify their carrier and confirm that each state's coverage requirements are met under the policy.

An EMR below 1.0 reduces your Utah workers' comp premium, while an EMR above 1.0 increases it. The EMR shows your actual claims history relative to expected losses for your industry class code. Utah employers can improve their EMR over time by reducing claim frequency, implementing safety programs and contesting inaccurate claims.

Sole proprietors and certain corporate officers in Utah may be able to exclude themselves from coverage under state law. Verify current opt-in and opt-out rules for your entity type with the Utah Labor Commission or a licensed insurance professional.

Workers' comp covers medical costs and lost wages for employees injured on the job without needing proof of employer fault. Employer's liability covers claims where an employee alleges that employer negligence caused the injury and pursues a lawsuit beyond the workers' comp system. Most Utah workers' comp policies include employer's liability coverage as Part Two of the policy.

Workers' comp claims affect your experience modification rate for three policy years in Utah, excluding the most recent completed year. A single large claim can raise your EMR and increase premiums for multiple renewal cycles.

MoneyGeek analyzed workers' comp insurance rates and provider performance across Utah using small business profiles with 1 to 4 employees spanning 408 major industries. Companies earn up to five points in each category in our scoring system. We then use a weighted average of these category scores to calculate a MoneyGeek score out of five.

- Affordability (55%): Based on average payroll for the most common employee code per industry and state classification, priced per employee for a 1 to 4 employee business.

- Customer Experience (35%): Evaluates buying (20%), which covers quote access, pricing accuracy and sales support; policy management (30%), which covers payroll reporting, audits, billing and loss control; and claims (50%), which covers FNOL speed, adjuster support, medical access, wage replacement and dispute handling.

- Coverage Options (10%): Assesses coverage completeness (35%), including employers' liability and wage and medical reimbursement; policy flexibility and endorsements (25%); eligibility, state and industry breadth (20%); and policy terms, limits and exclusions (20%).

About Connor Bolton

Connor Bolton is Senior SEO and Content Manager at MoneyGeek, where he leads the business and pet insurance editorial teams. He sets the research framework, data standards and content structure for his team. All content goes through his accuracy review before publication. Connor also writes in-depth guides and has spent more than four years covering insurance products across personal, commercial and specialty lines.

The research infrastructure Connor built covers auto, home, renters, life, health, business and pet insurance across pricing analysis, carrier research, customer experience and coverage evaluation. It includes over 6 million data points for business insurance across 408 industry areas, all 50 states and 16 vehicle types. The pet insurance side covers over 5 million profiles across 18 major providers, 100+ breeds and ages up to 20 years. Connor’s insurance research and his team's work has been cited by the U.S. Chamber of Commerce, Allstate, Liberty Mutual, CBS News, Forbes and LegalZoom.

Connor also talks with underwriters and carrier liaisons at Ethos, The Hartford, ERGO NEXT, Nationwide and State Farm, and monitors business and pet owner communities on Reddit. Those sources shape how his team evaluates carriers, structures rate analysis and writes for human buyers rather than search engines.

For questions about MoneyGeek's business and pet insurance content, contact him at connor@moneygeek.com or on LinkedIn.

Sources

- National Council on Compensation Insurance. "ABCs of Experience Rating." Accessed July 10, 2026.

- Utah Department of Insurance. "Workers' Compensation." Accessed July 10, 2026.

- Utah Labor Commission. "Employers' Guide to Workers' Compensation." Accessed July 10, 2026.

- Utah Legislature. "Utah Code Title 34A Chapter 2 Part 2." Accessed July 10, 2026.