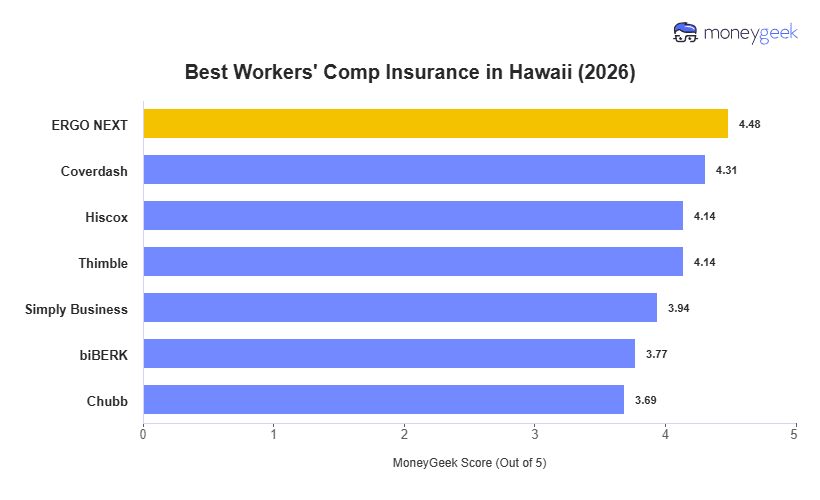

"ERGO NEXT leads Hawaii with the highest MoneyGeek score and the state's lowest rate at $109 per month. Coverdash earns the runner-up spot on the strength of its coverage score, the broadest policy options among Hawaii's seven ranked providers.

The $73 difference between ERGO NEXT ($109 per month) and Chubb ($182 per month) gives Hawaii employers a range of pricing options. This pricing gap shrinks in higher-risk industries such as construction, agriculture, and transportation, where loss costs are high across all providers.