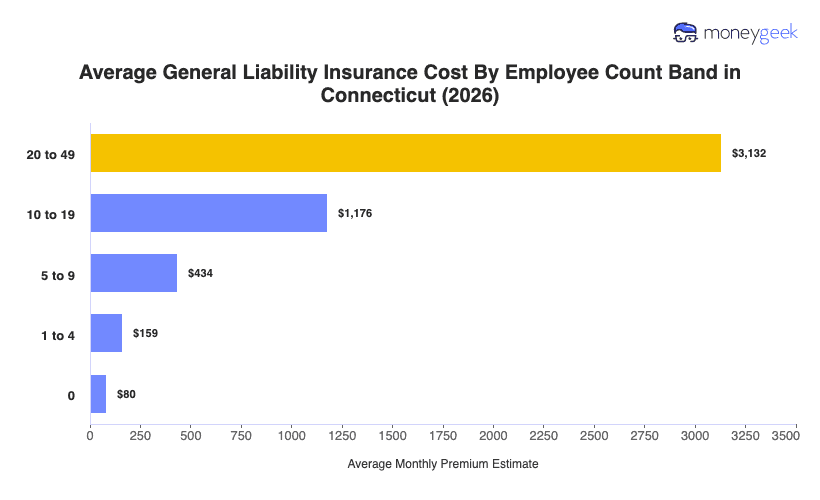

General liability insurance costs in Connecticut average $159 monthly ($1,906 annually) for businesses with one to four employees carrying limits of $1 million per occurrence/$2 million aggregate. This benchmark runs 29% above the national average of $123 monthly, placing Connecticut 45th nationally for affordability.

Connecticut is within a Northeast cost structure where rates vary across neighboring markets. Rhode Island averages $130 a month, Massachusetts $169 and New York $180.

Within the broader Northeast region, Maine ($112) and New Hampshire ($135) run $24 to $47 below Connecticut's benchmark. Connecticut sits in the upper-middle tier of this distribution, exceeding Rhode Island but remaining below both Massachusetts and New York.

Use this state average as a starting reference for understanding whether your quoted price falls within expected parameters given your operational profile, not as a prediction of your final premium. The Connecticut general liability insurance cost calculator below provides an estimate based on your specific business inputs.