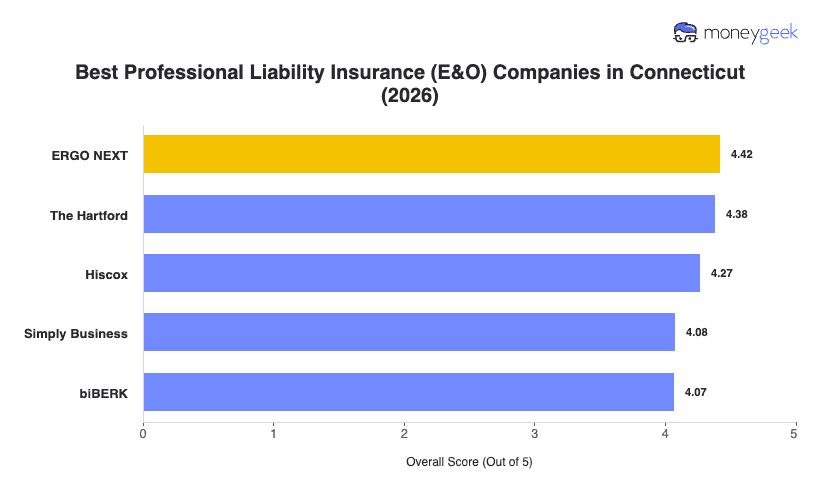

Our analysis of Connecticut professional liability insurers identified three providers that consistently outperformed the field on rates, service quality and coverage fit.

- ERGO NEXT: A fully online buying experience and broad industry coverage across Connecticut earned ERGO NEXT the top position. You can get a quote, buy a policy and access your certificate of insurance in about 10 minutes, which matters when a client contract is waiting. It ranks first across more than 10 industries in Connecticut including healthcare, construction, nonprofits, marketing, recreation and pet care, and it offers a bundling discount of up to 10% when you add professional liability to an existing policy.

- The Hartford: Deep roots in Connecticut's insurance industry and a strong track record with consultants, financial services firms and real estate professionals give The Hartford a clear second-place finish. The insurer has more than 200 years of experience and ranks first in Connecticut for beauty and wellness, cleaning, consulting, financial services and real estate. Healthcare providers and other professional services businesses will find better rates elsewhere, as The Hartford ranks ninth in both categories for the state.

- Hiscox: Broad profession coverage and 7-days-a-week phone support make Hiscox a reliable option for Connecticut businesses that want to talk to someone before buying. It ranks first for tech and hospitality professionals and second for consulting, financial services, nonprofits and pet care. Hiscox covers hundreds of professions and is a particularly strong fit for businesses that need industry-specific policy language rather than a generic E&O form.

These three providers suit most Connecticut businesses, but no ranked list covers every situation. Comparing business insurance options side-by-side and getting quotes directly gives you the clearest picture of what fits your business.