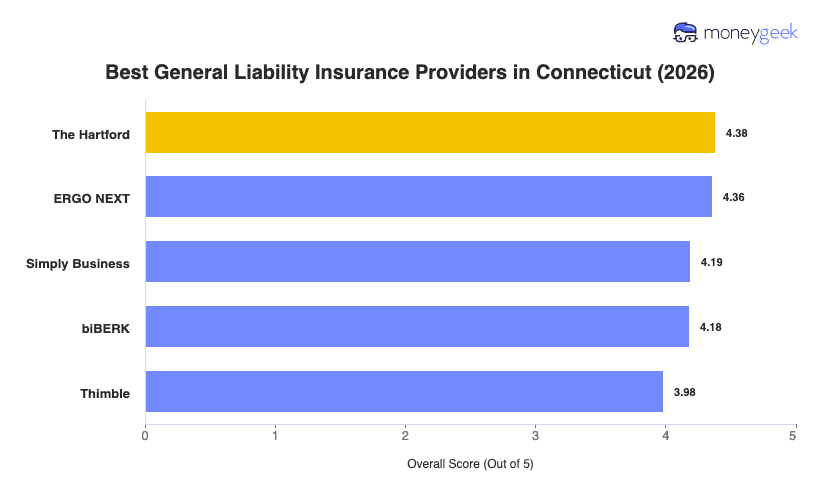

MoneyGeek analyzed general liability insurance options in Connecticut and identified five providers with strong small business coverage across the state's key industries, including hospitality venues near the coast and manufacturing operations in Naugatuck Valley:

- The Hartford: Best Overall, Best for Professional Services

- ERGO NEXT: Top for Customer Experience

- Simply Business: First-ranked for Comparing Multiple Carriers

- biBERK: Best for Service Businesses with Straightforward Needs

- Thimble: The best choice for Short-Term and On-Demand Coverage

The insurers below have strong track records in Connecticut and cover the business needs most common in the state. Here's how they compare: