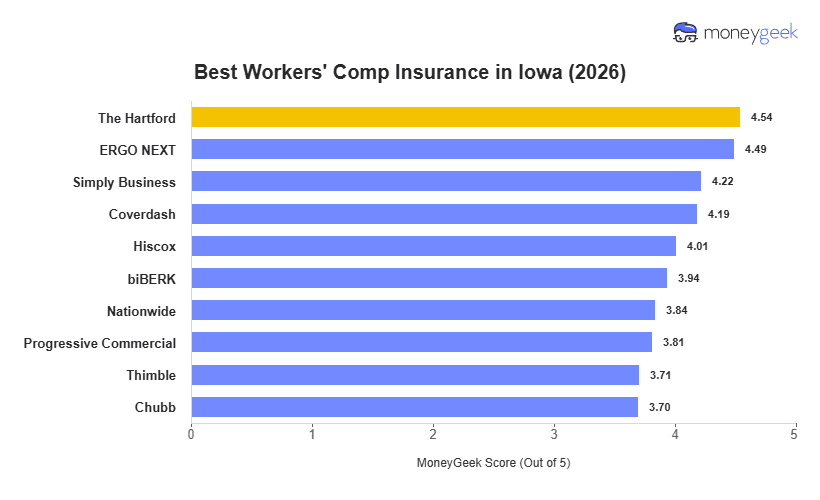

The Hartford leads Iowa's rankings with the top MoneyGeek score among workers' comp insurance providers in the state. ERGO NEXT is the runner-up, offering the lowest rate in the field.

ERGO NEXT is Iowa's cheapest provider at $53/month. Chubb is the most expensive at $91/month, a $38 spread. Low-hazard professional employers benefit most from that gap. The spread narrows for high-hazard class codes where underwriting tightens across all carriers.