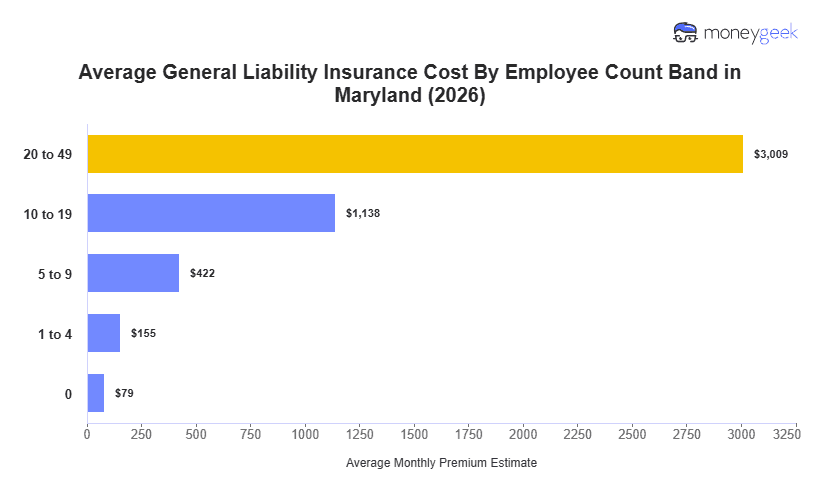

Maryland small businesses with one to four employees pay an average of $155 a month, or $1,859 a year, for general liability insurance. That benchmark is 26% above the national average, putting Maryland 44th for affordability.

Maryland's premiums are the highest among adjacent states and across the broader South Atlantic region. Pennsylvania, Delaware and Virginia range from $129 to $136 a month, $19 to $26 below Maryland. The gap widens regionally: West Virginia businesses pay roughly $87 a month, about half Maryland's benchmark. Florida, where insurance costs are elevated, comes in $11 a month lower. Maryland's position likely reflects its dense urban corridors, above-average litigation rates and higher commercial property values, all of which raise claim frequency and severity for insurers.

Actual premiums vary by industry classification, revenue, coverage limits and claims history. A quote near the Maryland average signals standard exposure for a small operation. A meaningful gap in either direction means one factor is pulling the number. The Maryland general liability insurance cost calculator below accounts for your specific business details and produces an estimate closer to your actual profile.