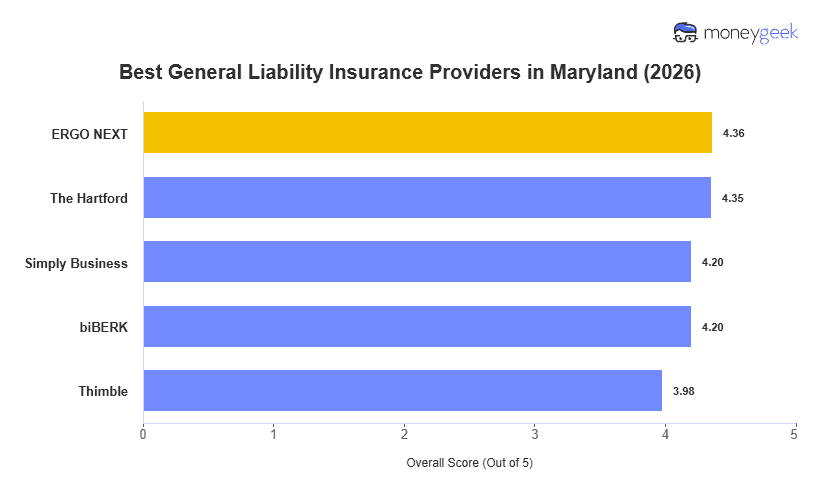

Every Maryland business has different coverage needs and budget constraints, so we evaluated 10 major general liability insurers across 408 business types using $1 million per occurrence/$2 million aggregate limits. These five providers emerged as the best and cheapest options for small businesses in the state.

- ERGO NEXT: Best Overall, Best for Service and Trade Businesses

- The Hartford: Best for Professional and Office-Based Businesses

- Simply Business: Best for Food and Childcare Businesses

- biBerk: Best for Fitness, Cleaning and Real Estate Businesses

- Thimble: Best for Project-Based and Gig Work

From an Annapolis charter boat operator to a Frederick landscaping company, Maryland businesses vary widely in risk and coverage needs. Review each provider's rates and rankings in the table below to see which one aligns with your business.