The average commercial auto insurance cost for Florida businesses is $230 per month ($2,763 per year) for minimum coverage, based on MoneyGeek's analysis of eight vehicle types across 25 general industry categories. That puts Florida well above the national benchmark of $163 per month and significantly higher than every neighboring state in the region.

Among nearby states, North Carolina comes closest to the national average at $164 per month, while South Carolina ($158), Georgia ($156) and Mississippi ($155) all run slightly below it. Tennessee ($145) and Alabama ($135) sit further below the benchmark.

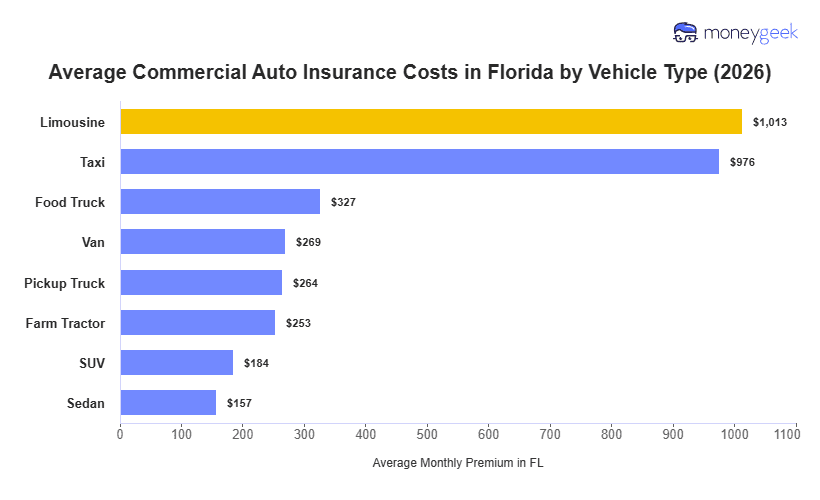

Commercial auto insurance rates in Florida are driven by the state's dense traffic, high litigation rates and above-average claim costs. Your commercial auto insurance rates will differ from that state benchmark depending on your vehicle, your drivers and what your business does.