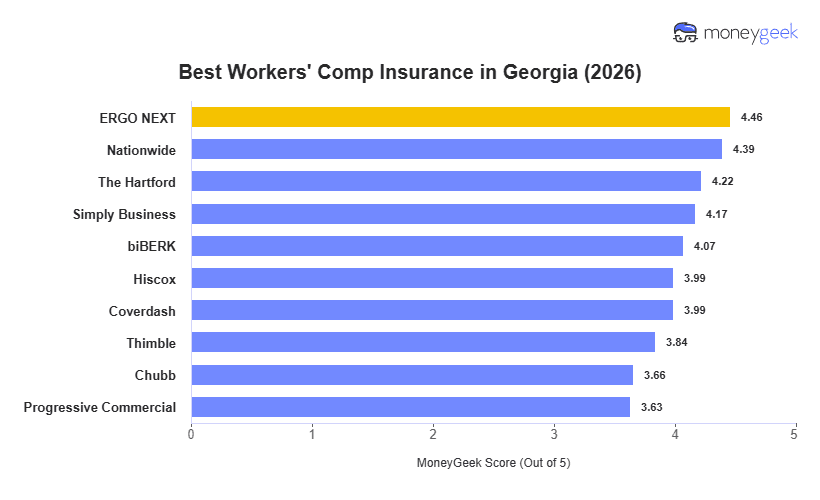

ERGO NEXT leads Georgia's workers' compensation market with the highest MoneyGeek score, combining the state's top customer experience rating with one of the lowest average monthly premiums. Nationwide ranks second with a nearly identical average rate but a lower overall score, trailing ERGO NEXT on customer service while outperforming it on coverage options.

Chubb averages $136 per month, a $57 gap above ERGO NEXT's rate. Employers in professional and service sectors have the most to gain from comparing costs and coverage across this range.