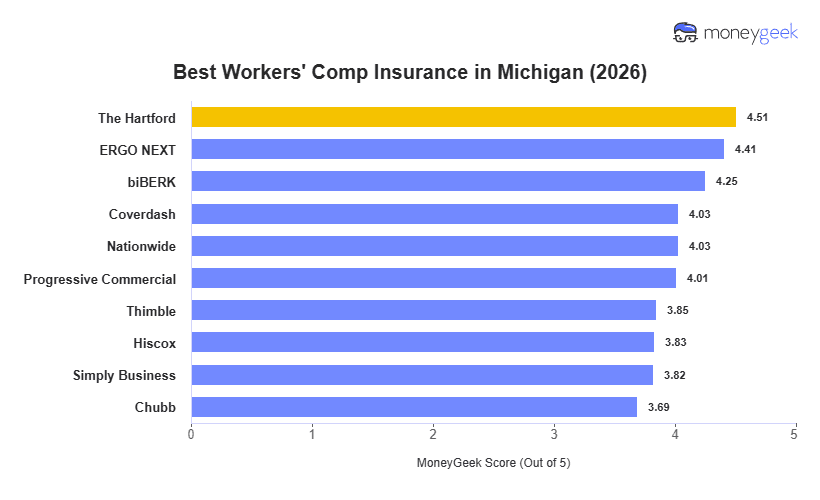

The Hartford is Michigan's best workers' comp provider with a MoneyGeek score of 4.51/5, driven by its strong affordability across a wide range of industries and reliable claims handling. ERGO NEXT and biBERK are solid runner-up options for Michigan businesses that prioritize competitive pricing and digital accessibility. MoneyGeek evaluated providers based on affordability, customer experience, and coverage breadth in the workers’ compensation insurance market.

The Hartford's $95 monthly rate and Chubb's $155 rate represent a $60 per employee monthly gap, a meaningful difference for small Michigan businesses in low-to-moderate injury industries. Businesses with straightforward payroll and clean loss histories benefit most from the cheapest providers, while Chubb's premium is justified for complex operations requiring specialty endorsements and dedicated risk management support.