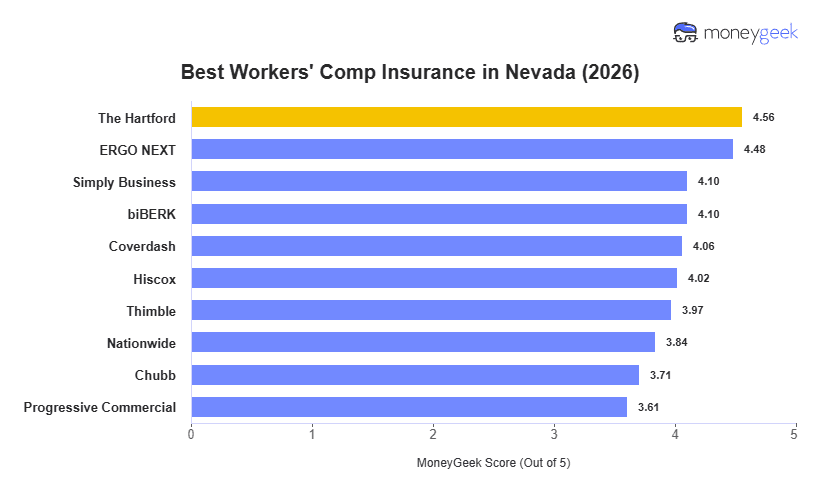

The Hartford is Nevada's best workers' comp insurance provider, with ERGO NEXT ranking second. It leads in customer experience and claims infrastructure. ERGO NEXT is the better fit for Nevada businesses that prefer a fully digital buying process.

There's a wide pricing gap between the cheapest and most expensive providers in our analysis. ERGO NEXT averages $74 per month, while Chubb averages $128, a $54 difference that adds up quickly for businesses with multiple employees. The gap is most pronounced in construction and hospitality, where risk levels and premiums are higher.