Contractor business insurance costs for tree service operations average $169 per month, or $2,026 per year, when measured across the most common coverage types your business is likely to carry. MoneyGeek's analysis drew from data across 50 states and Washington, D.C., covering courier services with one to four employees and standard policy limits of $1 million per occurrence and $2 million aggregate.

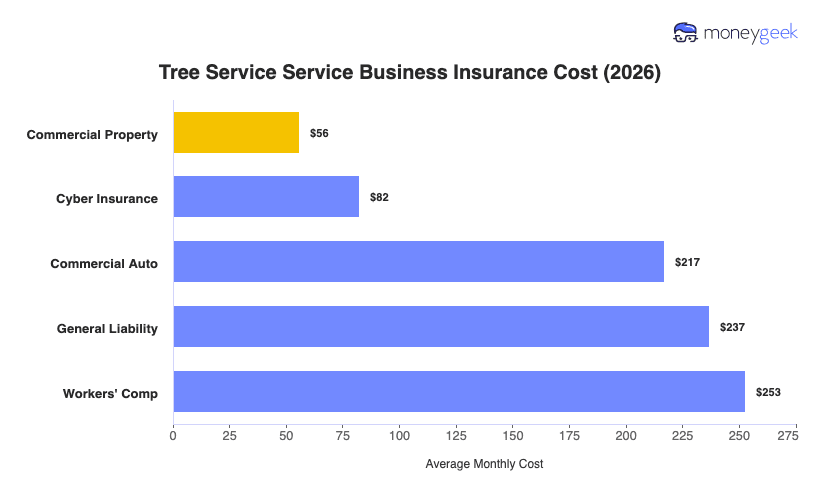

The cost varies considerably depending on which coverage type you're looking at, ranging from $56 to $253 per month. Commercial property sits at the lower end: if your business insures a fixed location like a yard, shed or equipment storage area, carriers price that at a defined replacement value. Workers' compensation anchors the upper end, driven by the nature of the work itself: aerial operation, chainsaw use and sustained exposure at height put tree service crews among the higher-risk classifications in the trades, and that risk profile is reflected in what carriers charge.

The table below shows average monthly and annual figures for each coverage type. Use them as benchmarks for setting expectations, not as quotes for your specific operation: