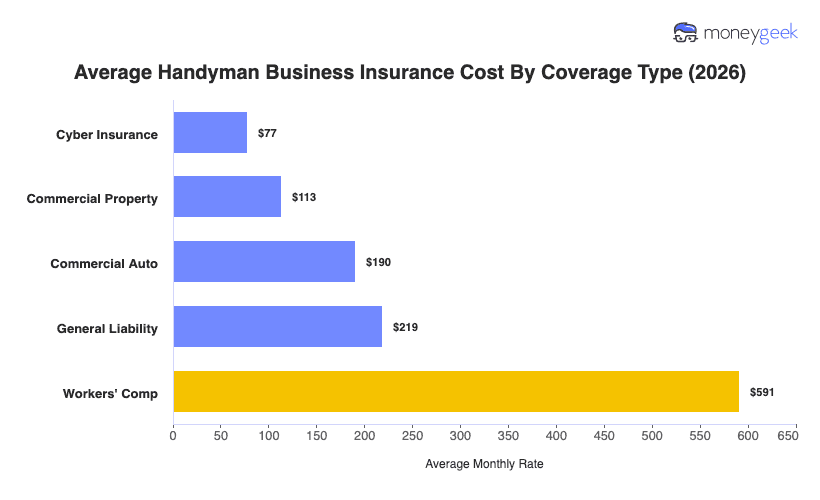

Handyman business insurance costs range from $219 to $1,225 per month, depending on the bundle you get. Most handymen need general liability, commercial auto and tools and equipment insurance, and puts your total at $440 per month. But if you have minimal tools, you might not need tools and equipment, bringing your cost down to $409 monthly.

When you start adding members to your crew, you'll need to get workers' comp, which adds $591 per month per employee. Traveling to multiple job sites adds to your risks, and cyber coverage covers your business if you accept online payments or send digital invoices. Larger jobs that involve multi-day rental-unit repairs, cabinet or door installation, small commercial repairs or permit-related work typically makes surety bonds part of your requirements. An expanded bundle, which costs $1,217 per month, includes all that.

We modeled these figures based on quotes for handyman businesses with one to four employees across all 50 states. When you request for quotes, several variables affect your actual rate, including which coverage types you include in your mix and their respective limits, where your business is based and your claims history, but you can use these averages to evaluate them.

I've detailed the handyman insurance bundles below and indicated how much each one costs on average: