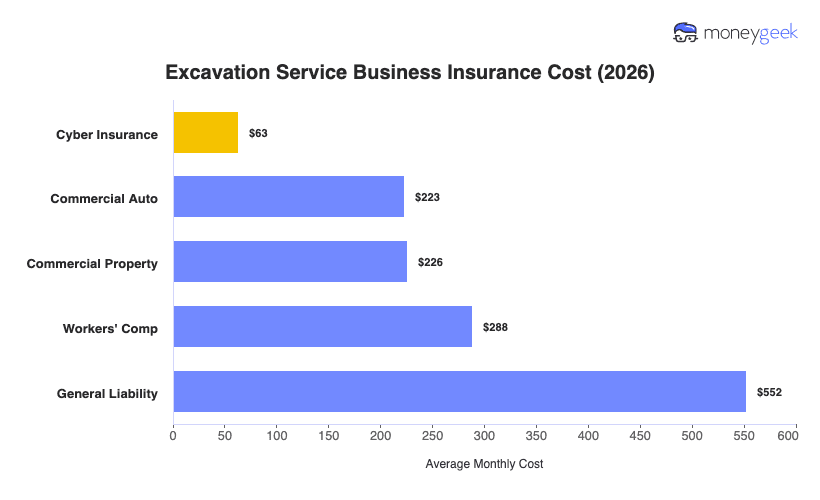

Contractor business insurance cost for excavation contractors average $271 per month, or $3,247 per year, across the five most common coverage types. MoneyGeek's analyzed quotes for businesses with one to four employees, $1 million per occurrence policy limits and across all 50 states and DC.

Individual policies range from $63 to $552 per month, with cyber coverage having the lowest estimate as most excavation operations carry a narrow digital footprint, centered on estimating software and bid platforms rather than large customer databases. General liability costs the most because excavation generates high-severity third-party claims, from utility strikes to ground disturbance damage on neighboring properties.

The figures below are benchmarks, not quotes, and your actual premium depends on your trade type, crew size and location.