In my analysis of painting contractor insurance costs, they sit on the lower end within their general industry category at 17th in affordability and 339th when compared to all other areas of work in my analysis. This translates to a monthly rate of $183/mo on average which is slightly lower than the national average for its work category of $190/mo, but much higher than the national average of $111/mo.

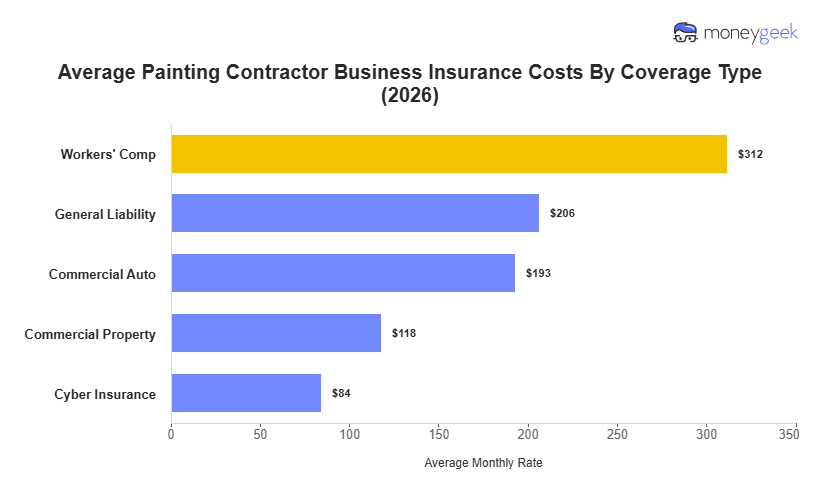

Like any other contracting work, rates are high at the coverage level for workers' comp ($312/mo per employee) and general liability policies ($206/mo) due to high levels of exposure with the public, the risks associated with frequent shifts in clients (especially in residential work), and the possibility of fall injuries while painting home exteriors or high-rise interior walls. Commercial property, cyber and commercial auto policies sit more modestly towards the center of the spectrum but can increase past benchmarks if you have more specialized equipment, store extensive customer data in any way and if you drive more frequently and for longer distances respectively.