Ecommerce businesses pay an average of $173 per month, or $2,080 per year, across five common coverage types. Retail business insurance costs vary widely across subindustries, and ecommerce sits at the least affordable end of all 39 we analyzed. These figures are modeled across businesses with 1 to 4 employees, $1 million per occurrence limits, and all 50 states plus DC.

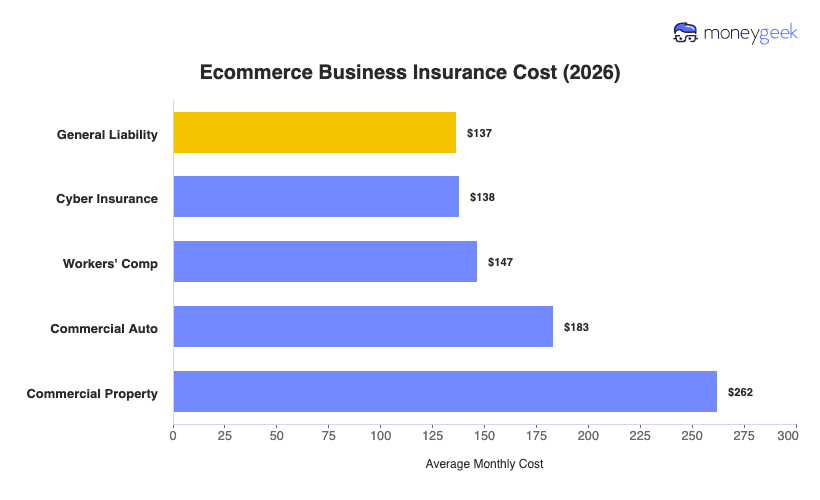

Individual policies range from $137 to $262 per month. General liability sits at the lower end, though ecommerce carries real product liability exposure from goods sold online. It prices lower because there's no physical storefront generating foot traffic and the bodily injury claims that come with it. Commercial property lands at the top because all your inventory sits in one place and a single loss event hits everything at once, and seasonal stock buildups push that exposure higher.

The breakdowns below are benchmarks rather than quotes, and your actual premium reflects your specific business profile.