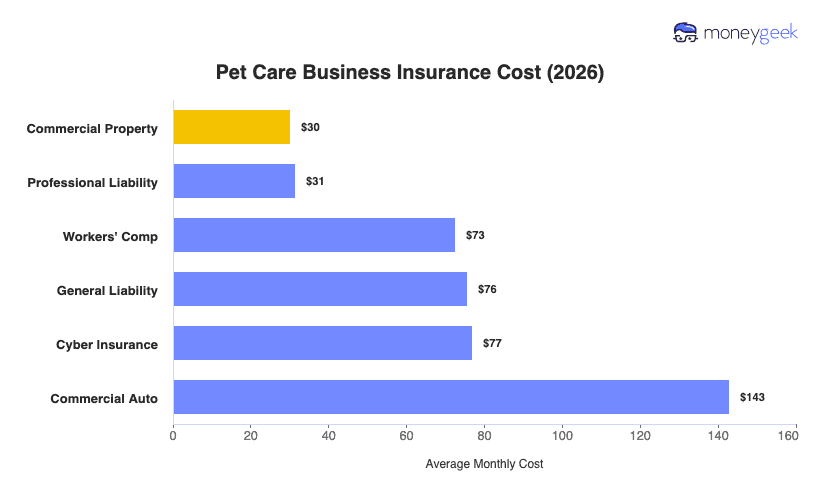

The average cost of business insurance for pet care services runs around $72 per month or $859 per year, averaged across the six most common coverage types. We modeled premiums for pet care services with one to four employees at standard $1 million per occurrence limits across all 50 states and DC.

Your individual policy costs range from around $30 to $143 per month depending on coverage type. You'll pay the least for commercial property coverage because your fixed-location equipment, from grooming tables and kennel runs to dryers, covers equipment with a clear replacement value rather than the unpredictable claim costs that push liability premiums higher. In comparison, commercial auto costs the most since a grooming van costs more to insure than a standard work truck because it travels to client locations, carries live animals and operates as both a vehicle and a workspace.

Use the figures below as benchmarks, not quotes since your actual rate depends on your business profile.