Restaurant insurance costs can range from about $249 to $859 per month, depending on the bundle that fits your coverage needs. For most full-service restaurants, the recommended bundle includes general liability, commercial property and workers’ compensation for one employee, averaging $283 per month. If you haven’t hired staff, your cost could be lower. If you have more employees, your premium increases because workers’ comp costs about $34 per employee per month.

If your restaurant keeps refrigerated inventory or depends on walk-in coolers, freezers, ovens and other key equipment, consider adding food spoilage and equipment breakdown coverage. That brings the full-service operations bundle to about $463 per month. If you also own a vehicle for deliveries, catering or supply runs and rely on online orders or digital payments, the expanded bundle costs about $859 per month.

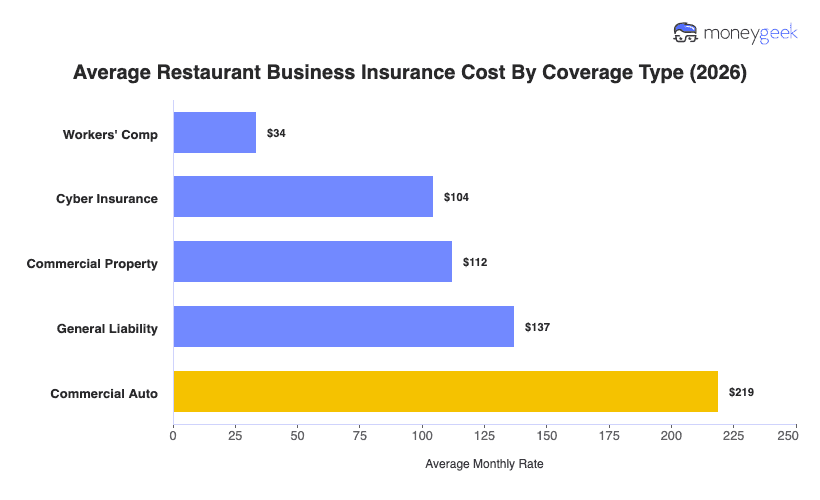

These figures are modeled averages based on quotes for restaurants with one to four employees across all 50 states, before discounts. Your actual premium can vary based on your state, claims history, and coverage limits, but these benchmarks give you a realistic range for evaluating your own quotes.

Below, I've broken down the different bundles and their corresponding costs: