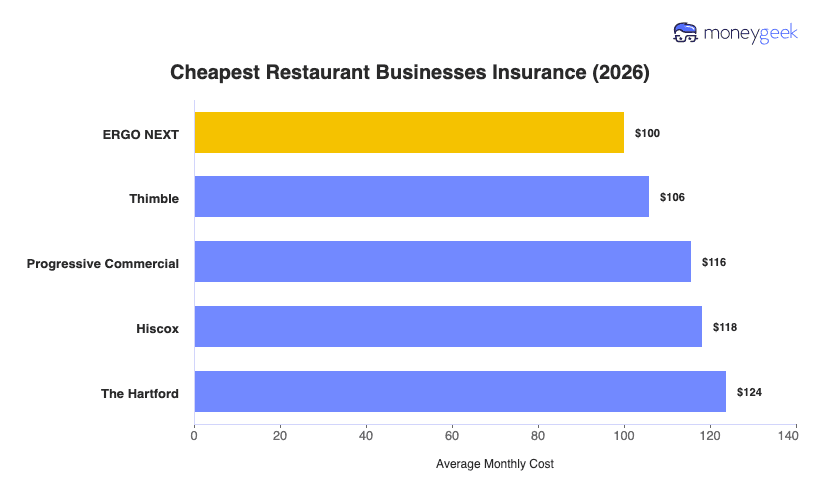

Full-service restaurants face more daily risk than most small businesses, from wet floors in the dining room to knife injuries in the kitchen to the liability that follows an over-served guest out the door. Finding affordable food business insurance is more within reach than many owners assume. ERGO NEXT leads at $100 per month, and the top three providers sit within $16 of each other. Nationwide and biBerk are the only two that price above the industry average.

Most providers in this market price below the industry average, and with the top three separated by just $16, none of them has a runaway price advantage. Whether you run a full bar with 20 servers or a 10-table BYOB with a small kitchen crew, your staffing structure and liquor service model will push your quotes toward different ends of that range.