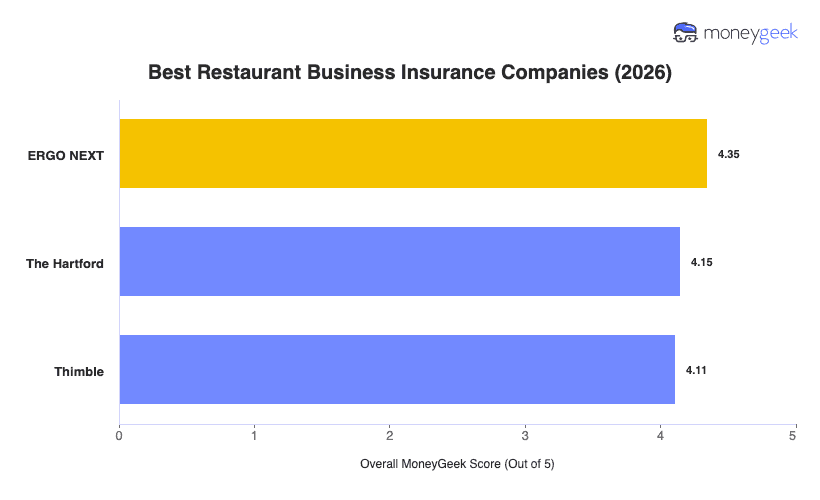

I analyzed price, coverage options and service quality across carriers to identify the best restaurant insurance companies. But the provider with the highest score isn’t automatically the right choice for your restaurant. If you run a small takeout shop, you likely care more about paying lower premiums and getting quick proof of insurance. A full-service restaurant typically needs broader coverage for employees, kitchen equipment, refrigerated inventory, alcohol service or delivery.

Use the table below to compare providers by fit, not just score. ERGO NEXT may be a better match if you run a smaller restaurant and want affordable coverage you can manage online. Thimble may fit better if you need insurance for a weekend pop-up, catering job or short-term food event.