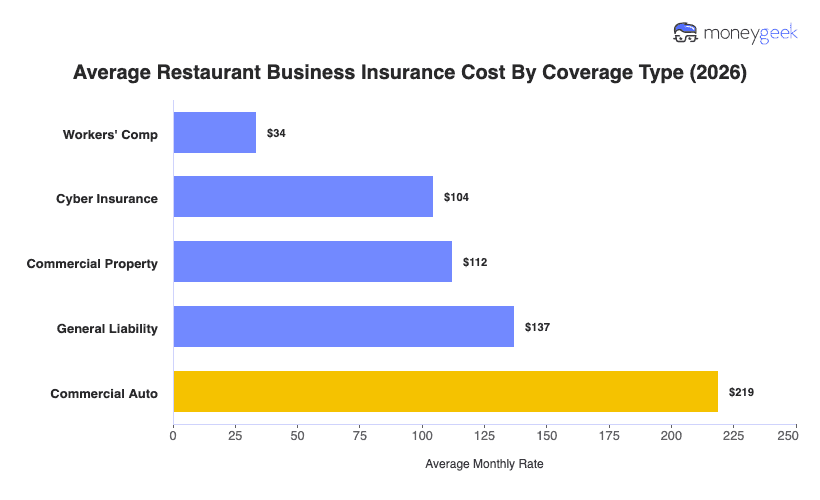

Restaurant insurance costs range from about $249 to $859 per month. The bundle that best fits your coverage needs determines where you fall within that range. For most full-service restaurants, the recommended bundle includes general liability, commercial property and workers' compensation for one employee, averaging $283 per month. Restaurants with no employees often pay less. Adding staff raises the premium, since workers' comp costs about $34 per employee per month.

Restaurants that keep refrigerated inventory or depend on walk-in coolers, freezers, ovens and other key equipment should add food spoilage and equipment breakdown coverage. That brings the full-service operations bundle to about $463 per month. Restaurants that also own a vehicle for deliveries, catering, or supply runs and rely on online orders or digital payments usually need the expanded bundle. That coverage costs about $859 per month.

These figures are modeled averages of quotes for restaurants with one to four employees across all 50 states, before discounts. Your actual premium depends on your state, claims history and coverage limits. Use this range as a starting point when you review your own quotes.

Here's how the bundles compare: