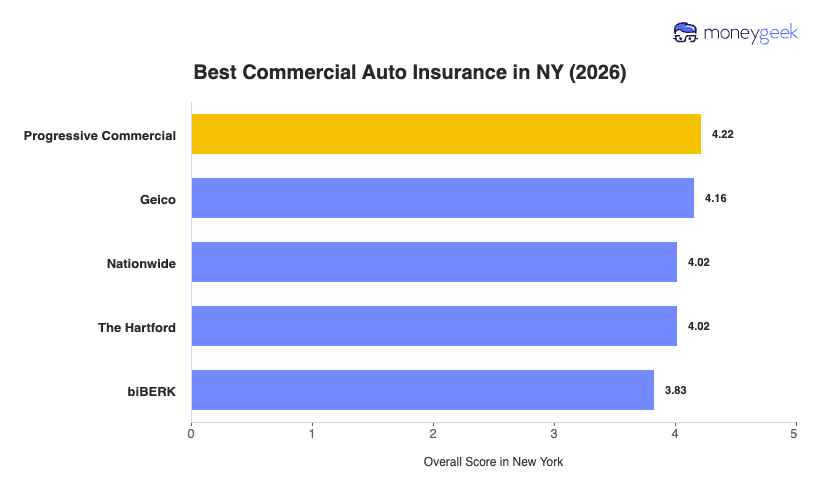

Based on our research, most businesses can find the best commercial auto insurance in New York with these providers:

- Progressive Commercial: Best Overall, Best for Fleet Operations

- GEICO: Best for Low-Risk Business Areas

- Nationwide: Best for Agricultural and Specialty Fleets

- The Hartford: Best for Coverage Depth

- biBerk: Best for Simple Coverage Needs

These five insurers cover the most common commercial auto needs New York businesses run into, from owner-operators running a single vehicle to multi-truck fleets crossing the state. Your best pick depends on your vehicle type, industry and the coverage depth your operation actually requires.