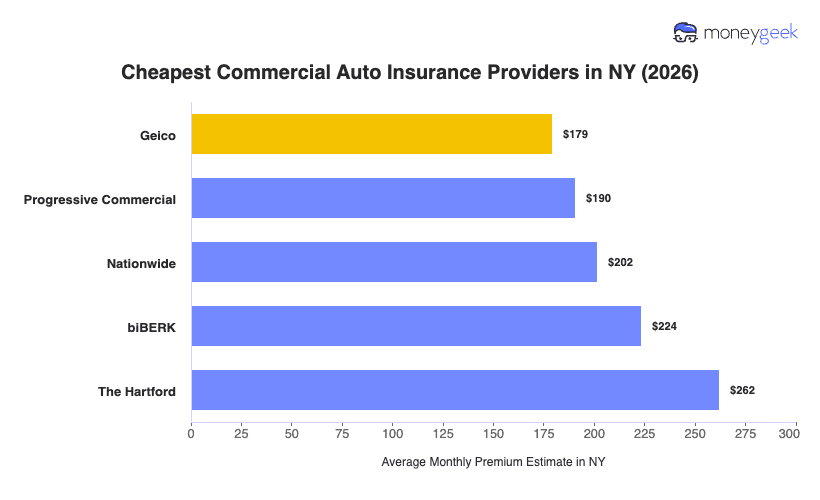

These are the cheapest commercial auto insurers in New York. GEICO leads on price overall, but the cheapest provider for you will depend on what your business actually does.

- GEICO averages $179 per month for commercial auto insurance in New York, 15% below the state average of $211 per month. It ranks first in affordability across 16 of 25 general industry categories in MoneyGeek's New York analysis, with its strongest savings for office-based, wellness and financial services businesses. New York businesses in consulting, financial services and marketing pay some of the lowest rates in MoneyGeek's data, with GEICO averaging $90 to $102 per month in those sectors.

- Progressive Commercial averages $190 per month in New York, 10% below the state average. It ranks first in affordability for eight general industry categories in MoneyGeek's New York analysis, including wholesale and distribution (31% below the industry average), transportation and logistics (26% below average) and manufacturing (25% below average). New York businesses in goods movement, food service and cleaning services will find Progressive Commercial's strongest pricing.

- Nationwide averages $202 per month in New York, 5% below the state average. It's the third-cheapest option overall in MoneyGeek's New York analysis and a reasonable starting point for businesses that don't fall into the specific industry profiles where GEICO or Progressive Commercial price lowest.

Actual New York commercial auto insurance costs vary by vehicle fleet details, driver records, services offered and location within the state, so these rankings won't apply to every New York business. Use these companies as a starting point to compare options and find the lowest-cost policy that meets your coverage needs.