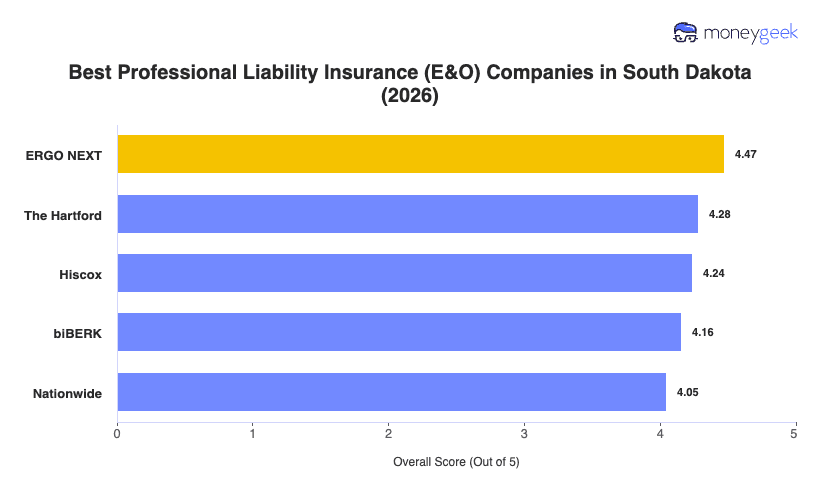

Our analysis of South Dakota professional liability insurers found three providers that consistently outperformed the rest on affordability, customer experience and coverage breadth.

- ERGO NEXT: The only provider in South Dakota to rank first across all three scoring categories simultaneously, affordability, customer experience and coverage. The buying experience is fully digital: quote, customize and share a certificate of insurance without a phone call, which suits the state's large base of independent contractors and small business owners. It ranks first in 12 of 18 industries in the state, but consulting, financial services and education are better served elsewhere.

- The Hartford: Its strength is depth over breadth. It ranks first in South Dakota for financial services, consulting, hospitality and marketing and communications, meaning its policy terms fit client-intensive, contract-driven work particularly well. Its complaint volume runs below the national average and it brings more than 200 years of claims experience behind every decision. Healthcare and other professional services are weaker fits, where it ranks ninth in the state.

- Hiscox: Built exclusively for small businesses, it covers more than 180 professions and structures policies around each industry's actual risk profile rather than a generic template. It ranks first in South Dakota for nonprofits and second for fitness, childcare, beauty and wellness, hospitality and pet care businesses. Bundling two or more Hiscox policies earns a 5% discount.

Ranked providers represent the best fit for most South Dakota businesses, but no single list accounts for every industry or client contract requirement. Comparing business insurance options side-by-side and pulling quotes directly from carriers gives you the clearest picture.