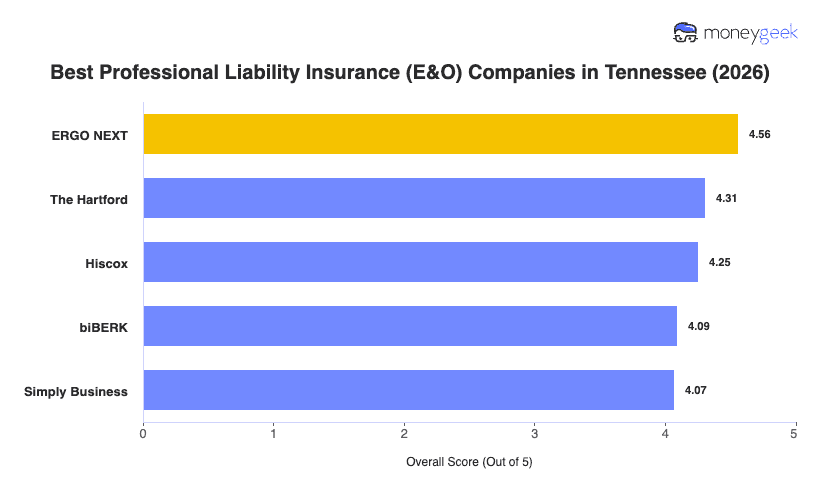

Our analysis of Tennessee professional liability insurers identified three providers that performed well on rate, coverage quality and customer experience.

- ERGO NEXT earned the top spot in Tennessee partly because of its fully digital platform: quote, bind and get a shareable certificate of insurance in about 10 minutes. It covers more than 1,300 business types and has the lowest rates across 12 Tennessee industries, including consulting, financial services, health care, real estate, construction and cleaning services. Tennessee businesses in higher-risk hospitality categories (lodging and food spoilage) and certain construction operations should verify whether their work is covered before buying. ERGO NEXT excludes some professional negligence exposures in those categories.

- The Hartford brings more than 200 years of underwriting experience and a dedicated claims specialist structure that most newer insurers don't have. It ranks first or second in Tennessee for beauty and wellness, hospitality, marketing, arts and real estate, though Tennessee health care businesses and other professional services firms should look at alternatives: The Hartford ranks ninth in Tennessee in both of those segments. Its business owner's policy (BOP) pairs professional liability with general liability and commercial property coverage, a good fit for established Tennessee businesses that want one consolidated policy.

- Hiscox responds immediately to any covered claim, regardless of merit. It ranks first or second in Tennessee across tech/IT, nonprofits, financial services, consulting, fitness, childcare, hospitality and pet care. Its worldwide coverage on U.S.-filed claims means Tennessee businesses working across state lines or internationally have the same coverage they'd have for domestic work.

The ranked providers are the strongest fit for most Tennessee businesses, but no ranking captures every variable your business brings. Get quotes directly from each insurer and compare options side-by-side before you commit.