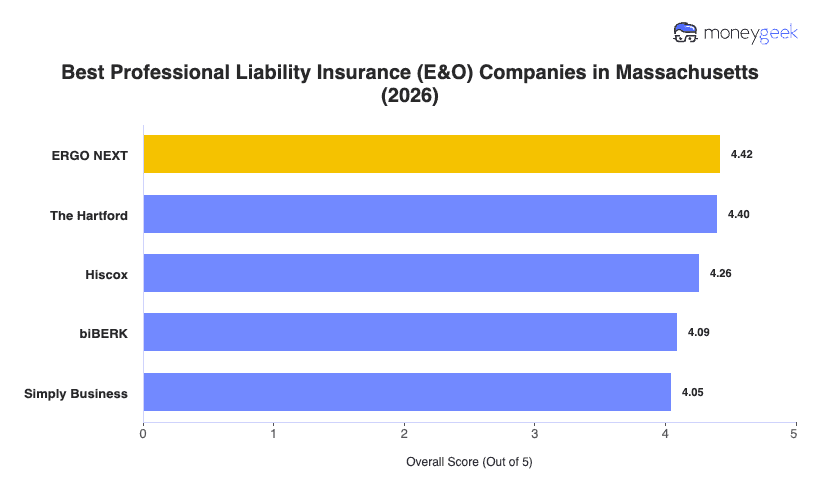

Our analysis of Massachusetts professional liability insurers found three providers that consistently outperformed the field on rates, coverage breadth and customer experience.

- ERGO NEXT: A fully digital buying experience that delivers quotes in under six minutes, instant certificates of insurance and 24/7 policy access through a highly rated mobile app earned ERGO NEXT the top position. The insurer ranks first in Massachusetts for healthcare, pet care, construction, real estate, fitness, recreation, nonprofit and arts/media industries. Financial services and consulting businesses should compare other options, as ERGO NEXT ranks sixth in both categories for Massachusetts.

- The Hartford: Profession-specific coverage depth and a structured claims process set The Hartford apart from faster-moving digital competitors. It ranks first in Massachusetts for beauty and wellness, cleaning services, consulting, financial services, hospitality and marketing, with particularly strong affordability scores in those categories. Healthcare and other professional services businesses will find better fits elsewhere, as The Hartford ranks ninth in both for this state.

- Hiscox: Coverage across more than 180 professions and policy language broader than most commodity E&O products make Hiscox the right call for Massachusetts businesses that don't fit a standard box. The insurer ranks first in Tech/IT for Massachusetts and holds second-place rankings in hospitality, consulting, financial services and real estate, backed by over a century of specialty underwriting experience.

Ranked providers represent the strongest fit for most Massachusetts businesses, but no list covers every situation. Comparing business insurance options side-by-side and getting direct quotes gives you the clearest picture of what each provider actually costs and covers for your specific work.