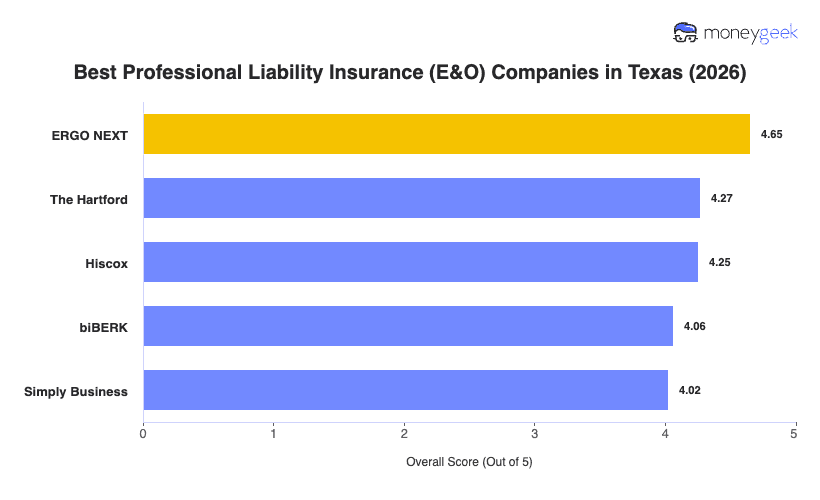

Our analysis of Texas professional liability insurers identified three providers that consistently outperformed the field on rates, coverage quality and customer experience.

- ERGO NEXT: A fully digital buying experience, quotes that bind in about 10 minutes and 24/7 certificate of insurance access through its app put ERGO NEXT at the top for most Texas small businesses. It ranks first in 15 of 18 Texas industries in our study. Texas contractors and hospitality operators should note that ERGO NEXT excludes construction-related operations and higher-risk hospitality work from professional negligence coverage.

- The Hartford: Claims handling depth and specialist support drive its Texas rankings, where it takes the top spot for real estate and hospitality and travel businesses and ranks second for marketing, communications and education firms. Texas healthcare providers and other professional services businesses will find it ranks ninth in those industries, making it a weaker fit there.

- Hiscox: Its professional liability policies cover work performed anywhere in the world, with claims filed in the U.S. or Canada, which suits Texas businesses with out-of-state clients. Hiscox ranks first for childcare and second across consulting, financial services, tech/IT and nonprofits.

These three providers represent the best fit for most Texas businesses, but no ranked list accounts for every situation. Comparing business insurance options side-by-side and getting direct quotes gives you the clearest picture.