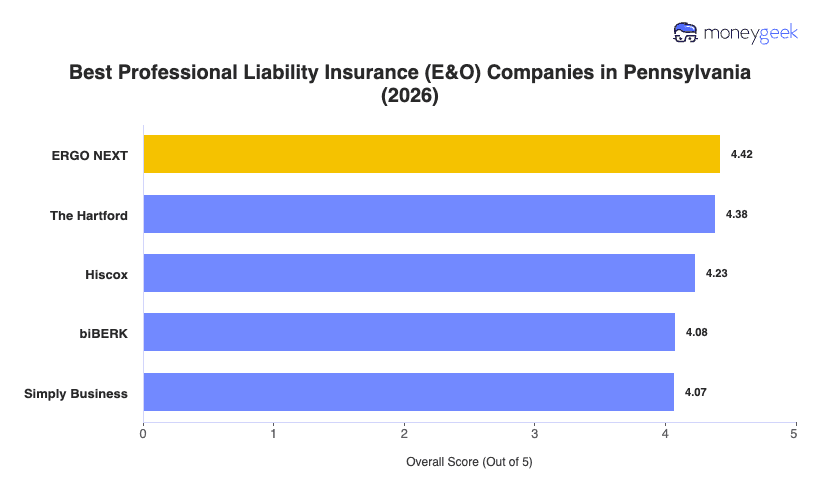

Our analysis of Pennsylvania professional liability insurers identified three providers that outperformed the field across affordability, coverage quality and customer experience.

- ERGO NEXT: A digital-first buying experience and strong performance across the widest range of industries earned ERGO NEXT the top spot in Pennsylvania. The insurer ranks first for professional liability in healthcare, real estate, pet care, fitness, arts and media, and recreation, a breadth that suits small Pennsylvania businesses across Philadelphia's service economy and Pittsburgh's growing healthcare sector. It also offers near-instant coverage binding, which matters when client contracts require proof of insurance quickly.

- The Hartford: Profession-specific coverage options and a long track record serving small to mid-size firms set The Hartford apart, particularly for Pennsylvania's consulting, financial services, tech and marketing businesses, where it ranks first for affordability. With more than 200 years of insurance experience, it brings dedicated claims support and risk management resources that newer digital carriers don't offer. Pennsylvania businesses in healthcare or other professional services should note The Hartford ranks 9th in those categories, so it's a stronger fit for the industries where it leads.

- Hiscox: Broad industry coverage and strong digital quoting make Hiscox a reliable third option for Pennsylvania businesses, with particular strength in childcare, consulting, financial services, nonprofit and tech. Solo practitioners and firms under 10 employees benefit most from its streamlined application process and flexible coverage options.

Ranked providers represent the best fit for most Pennsylvania businesses, but no list covers every situation your business has. Comparing business insurance options side-by-side and getting quotes directly from carriers gives you the clearest picture of what works for your specific industry and risk profile.