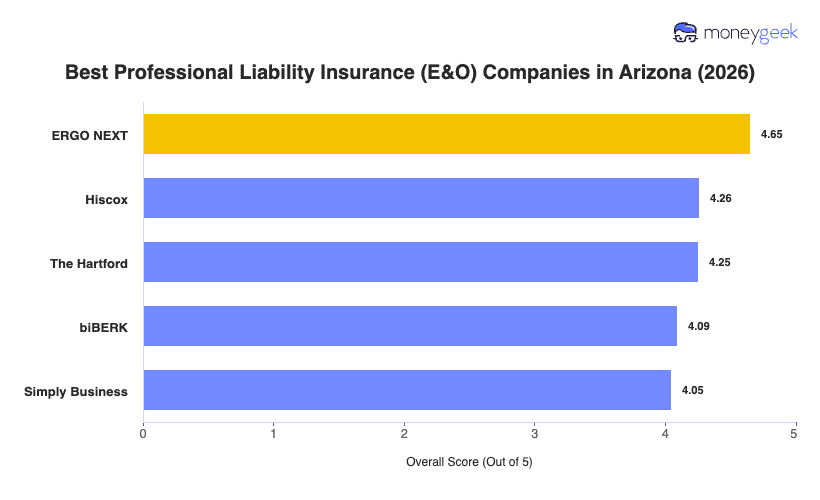

Our analysis of Arizona professional liability insurers found three providers that outperformed the field across affordability, customer experience and coverage breadth.

- ERGO NEXT: A digital-first buying experience and broad coverage across Arizona's hands-on and B2C industries put this insurer at the top spot. Backed by Munich Re following its 2026 rebrand, the insurer offers 24/7 policy access and AI-powered instant quoting that most carriers still can't match. It ranks first in overall score across 15 of 18 industries in Arizona, making it a strong fit for cleaning services, construction contractors, childcare providers, fitness businesses and pet care operators statewide.

- Hiscox: Industry depth earned Hiscox a strong second, with professional liability coverage tailored across more than 180 professions and a one-business-day claims response target that puts it ahead of most competitors on service speed. Arizona nonprofits, financial services firms and tech consultants all benefit from the insurer's specialty policy structure, and its 125-year operating history gives it underwriting precision that newer carriers don't bring to the table.

- The Hartford: Claims processing speed sets The Hartford apart at third, with some claims resolved in as few as five days and a customer experience score that ranks second among all providers in this analysis. It earns the top spot in Arizona's Hospitality, Travel and Tourism industry. Arizona businesses in healthcare and other professional services should note that the insurer ranks lower in those categories and may find a closer fit with another provider.

Ranked providers represent the strongest match for most Arizona businesses, but no single list accounts for every profession, client type or risk profile your business carries. Comparing business insurance options side-by-side and requesting quotes directly from each carrier gives you the clearest read on what you'll actually pay.