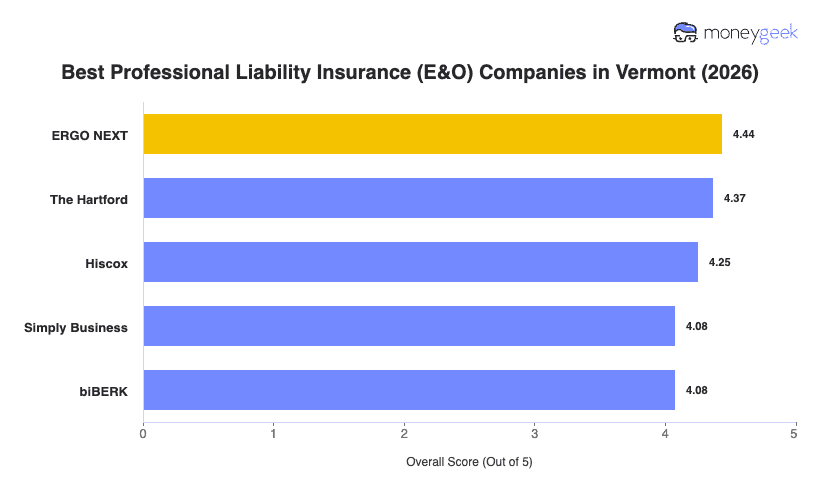

Our analysis of Vermont professional liability insurers found three providers that consistently outperformed the field on overall score, coverage quality and customer experience.

- ERGO NEXT: Fully digital from quote to certificate, with 24/7 self-service and instant proof of insurance that Vermont's small business owners can share with clients without calling anyone. ERGO NEXT ranks first in Vermont across a wide range of industries including healthcare, construction, tech, pet care, recreation and arts and media. Consulting and financial services businesses will find better fits elsewhere, as those industries score notably lower for this provider.

- The Hartford: A claims handling track record that few carriers can match earned The Hartford the second spot. It draws 22% fewer complaints than the national average for its size, and its professional liability coverage can be added directly onto a BOP, which simplifies coverage management for Vermont businesses that need both. The Hartford is the strongest pick in Vermont for consulting and financial services firms, though healthcare and other professional services businesses should compare options carefully before committing.

- Hiscox: Over 125 years of specialty insurance experience backs Hiscox's E&O policies, which cover more than 180 professions and go particularly deep for white-collar businesses like IT consultants, accountants, architects and nonprofits. Vermont hospitality and travel businesses rank Hiscox first in the state, and its all-digital buying process gets you a certificate of insurance in minutes.

These three providers are the strongest fit for most Vermont businesses, but no ranked list covers every situation. Comparing business insurance options side-by-side and pulling quotes directly from each carrier gives you a clearer picture than any ranking alone.