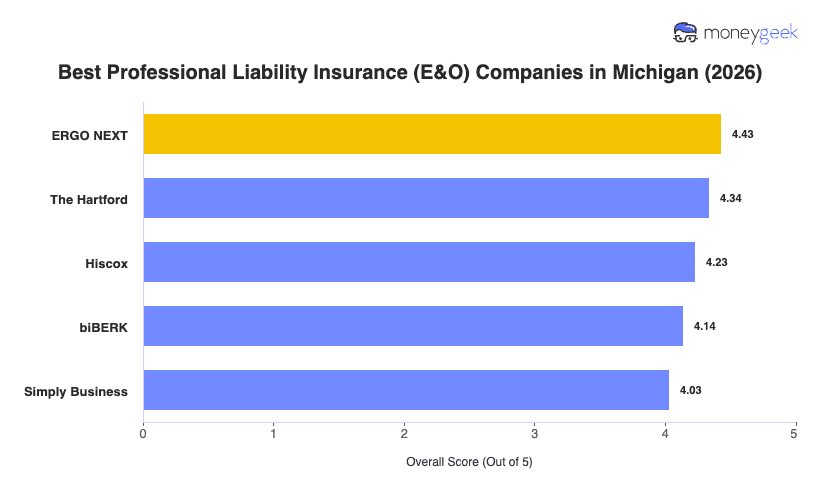

Our analysis of Michigan professional liability insurers found three providers that consistently outperformed the field across affordability, customer experience and coverage quality.

- ERGO NEXT: Ranking first across 12 of 18 Michigan industry categories, including health care, construction, real estate and tech, this insurer delivers the broadest coverage reach in the state. The buying process is fully online and built for speed, making it a strong fit for solo practitioners and small firms that don't want to work through a broker. Michigan professionals in consulting, financial services and education should weigh other options, as ERGO NEXT ranks sixth, sixth and seventh respectively in those categories.

- The Hartford: Deep specialization in consulting, financial services and hospitality gives The Hartford a clear edge for Michigan businesses in those industries, where it ranks first overall. With more than 200 years in the insurance market, it brings dedicated specialist support and risk management resources that newer carriers don't offer. The insurer underperforms for health care and other professional services providers, ranking ninth in both categories for Michigan.

- Hiscox: Nonprofit organizations and tech firms in Michigan get particularly strong performance from Hiscox, which ranks first for nonprofits and second for tech/IT statewide. The insurer covers virtually every industry that needs professional liability coverage and offers 24/7 policy support, which matters for businesses that operate outside standard business hours. Construction professionals should look elsewhere, as Hiscox ranks seventh in that category for Michigan.

The providers above represent the best fit for most Michigan businesses, but no ranking accounts for every variable your operation brings. Comparing business insurance options side-by-side and pulling quotes directly from carriers gives you the clearest picture of what you'll actually pay and what you'll actually get.